LTIMindtree Merger: Synergistic Growth Potential

Updated: 30 May 2023 • 5:32 pm

Posted by:

[vc_row type="in_container" full_screen_row_position="middle" column_margin="default" column_direction="default" column_direction_tablet="default" column_direction_phone="default" scene_position="center" text_color="dark" text_align="left" row_border_radius="none" row_border_radius_applies="bg" overflow="visible" overlay_strength="0.3" gradient_direction="left_to_right" shape_divider_position="bottom" bg_image_animation="none"][vc_column column_padding="no-extra-padding" column_padding_tablet="inherit" column_padding_phone="inherit" column_padding_position="all" column_element_spacing="default" background_color_opacity="1" background_hover_color_opacity="1" column_shadow="none" column_border_radius="none" column_link_target="_self" column_position="default" gradient_direction="left_to_right" overlay_strength="0.3" width="1/1" tablet_width_inherit="default" tablet_text_alignment="default" phone_text_alignment="default" animation_type="default" bg_image_animation="none" border_type="simple" column_border_width="none" column_border_style="solid"][vc_column_text css=".vc_custom_1685448133407{margin-right: 16px !important;margin-left: 16px !important;border-right-width: 10px !important;border-left-width: 10px !important;}"]LTIMindtree was formed due to the merger of two mid-sized IT services companies, L&T Infotech (LTI) and Mindtree resulting in the merged entity being the fifth largest IT services company by market capitalisation. Its services include digital solutions with focus on select verticals such as BFSI, Retail, Travel & Hospitality, Manufacturing & Resources, Health and Hi-Tech.

The merger process was completed in Q2FY23 and from FY24, it has started operating under a unified system and processes. This will provide potential revenue and cost synergies, which are expected to boost margin expansion in future. This along with operational synergies in diversified capabilities will create cross-sell and up-sell opportunities. The enhanced scale benefits will provide competitive advantage while participating in large deals.

Highlights of Q4FY22 and FY23 results

- Q4FY23 Revenue at $1,057.5 million (growth of 11.9% YoY) and net profit at $135.6 million (decline of 7.8% YoY).

- Q4FY23 INR Revenue at Rs 86,910 million (growth of 21.9% YoY) and net profit at Rs 11,141 million (growth of 0.5% YoY).

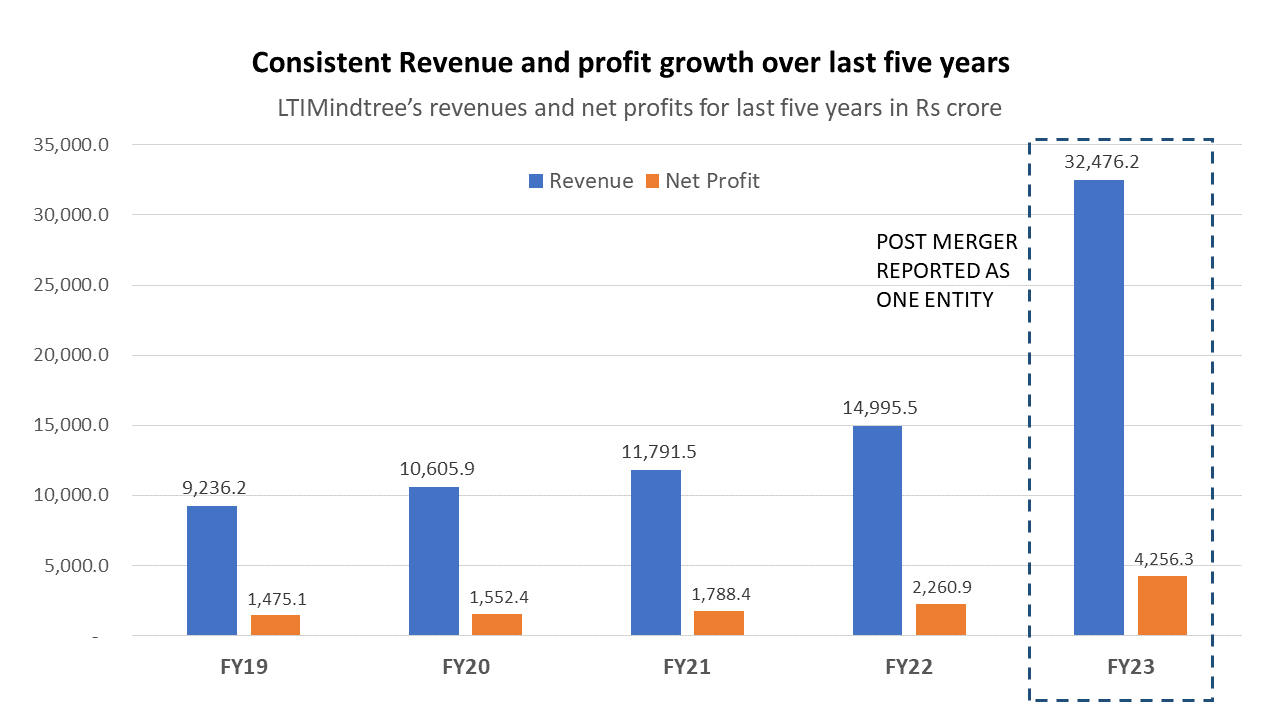

- FY23 Revenue at $4,105.7 million (growth of 17.2% YoY) and net profit at USD 545.7 million (growth of 3.0% YoY).

- FY23 INR Revenue at Rs 3,31,830 million (growth of 27.1% YoY) and net profit at Rs 44,103 million (growth of 11.7% YoY).

- The company during Q4FY23 added 31 new clients. Also, on a QoQ basis it added two clients to US$50 mn + and one client to US$20 mn + revenue deals.

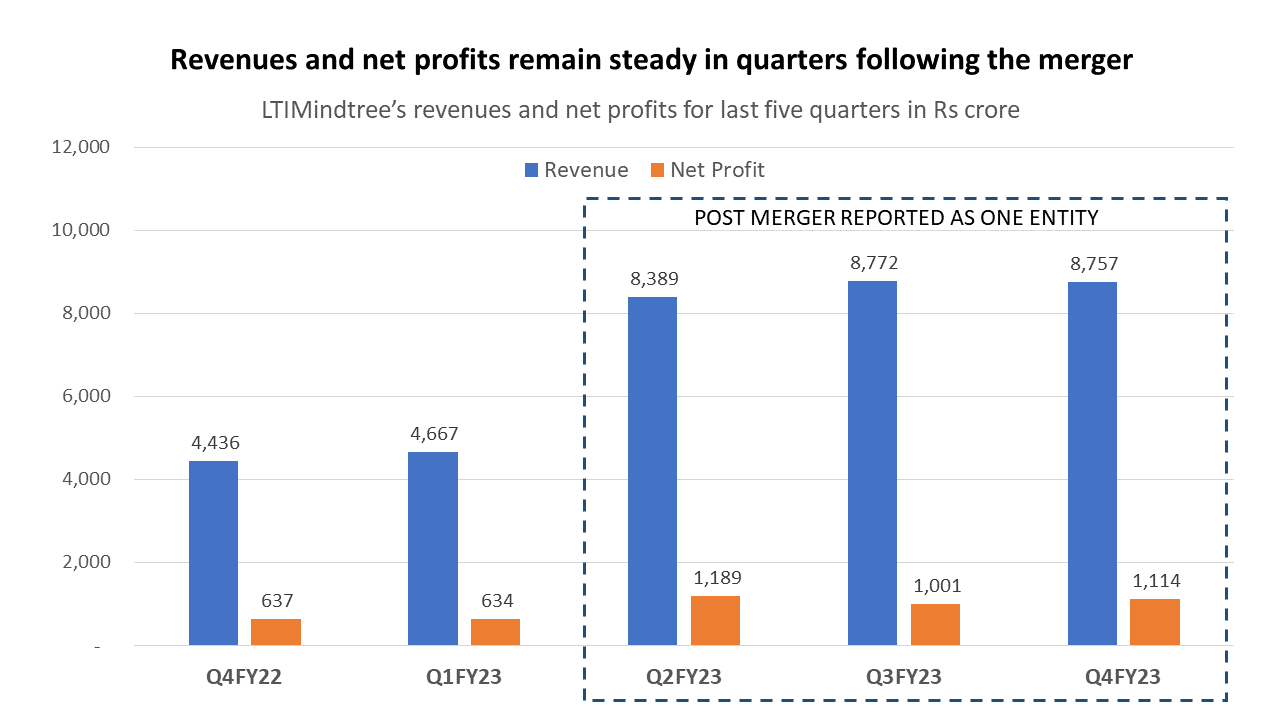

Merged entity posts stable set of numbers

Post completion of the merger in Q2FY23, the numbers were reported for the integrated entity, and these have been stable for the last three quarters. In case of mergers, deviations on some metrics are likely to occur due to one of the companies. However, in this case, the merged entity has not shown any major red flags over the last two quarters and there is no major decline either. With the integration complete in all aspects, the company is in a stronger position.

The EBIT margin of the company improved by 2.5% QoQ to 16.4% in Q4FY23. The company indicated that margin improvement was achieved on account of the increased operational efficiencies due to the merger. A reduction in headcount (~1,916) was majorly attributed to the reduction in lateral hires and as a combined entity, the company had enough bench strength to redeploy talent.

LTIMindtree said that Q4 performance was impacted due to slower execution of deals due to delayed start to some of the projects, which it won recently. The company indicated that it is seeing a spill-over of the same in Q1FY24 and recovery is expected from Q2FY24 onwards.

LTIMindtree reported an EBIT margin 16.2% in FY23 as compared to EBIT margin of 17.8% in FY22. The company mentioned that it is guiding for double digit revenue growth in FY24 and the confidence of the same is coming from a few favourable factors. One being the deal pipeline is healthy and the company does not see any major issue there. Secondly the order book continues to be healthy and currently stands at US$4.87 bn.

On the results, Debashis Chatterjee, CEO and Managing Director of LTIMindtree said, “This industry-leading performance positions us well to deliver continued profitable growth in FY24. As we move to unified systems & processes, we are ready to exploit the synergies. Our Q4 revenue came in at a healthy USD 1.06 billion – up 13.5% year-over-year in constant currency and 11.9% in reported USD terms. Our order inflow for the quarter came in at USD 1.35 billion, helping us close the full-year order inflow at USD 4.87 billion. We added 31 new clients for Q4 and increased our count of USD 50 million plus customers by 2 to 13. Our full-year operating margin was at 16.2% and the basic EPS was at INR 149.1. Client requirements have changed over the last quarter, and we are now meeting the new requirements to deliver cost savings which are being directed to fund in-flight transformation programs.”

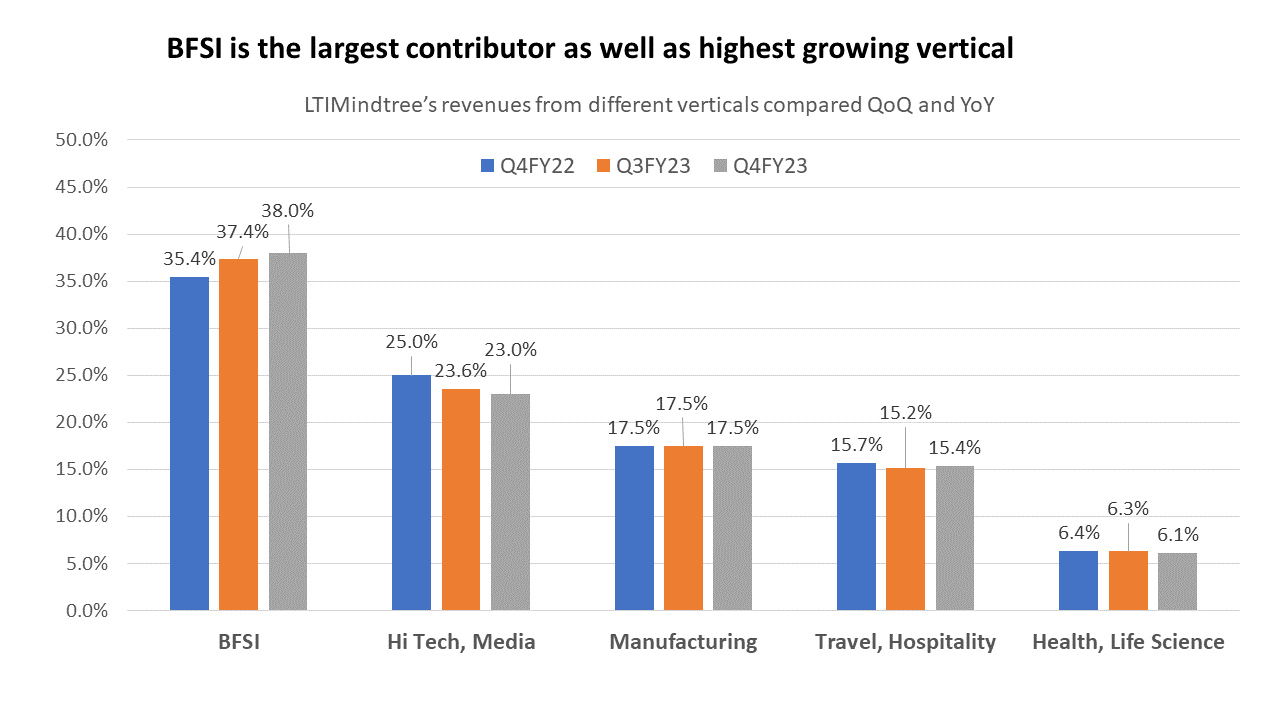

Vertical wise BFSI (38% of mix) grew 2.7% QoQ while retail & manufacturing reported growth of 2.4% & 1% QoQ, respectively. Hitech & Health declined for a second straight quarter reporting a decline of 1.5% & 2.2%, respectively

LTIMindtree is among the few IT companies that has managed to grow its BFSI vertical QoQ as well as YoY basis. This is the largest revenue contributing vertical and the growth of this bodes well for the company.

The company said that as its clients are now focusing on costs, thereby incremental pipeline is coming from cost take out deals and the trend is likely to continue till inflation pressures ease off. LTIMindtree also said that it is seeing strong opportunities in the BFSI space despite a couple of clients freezing some of the programs. It is expecting recovery in BFSI space from Q2FY23 onwards.

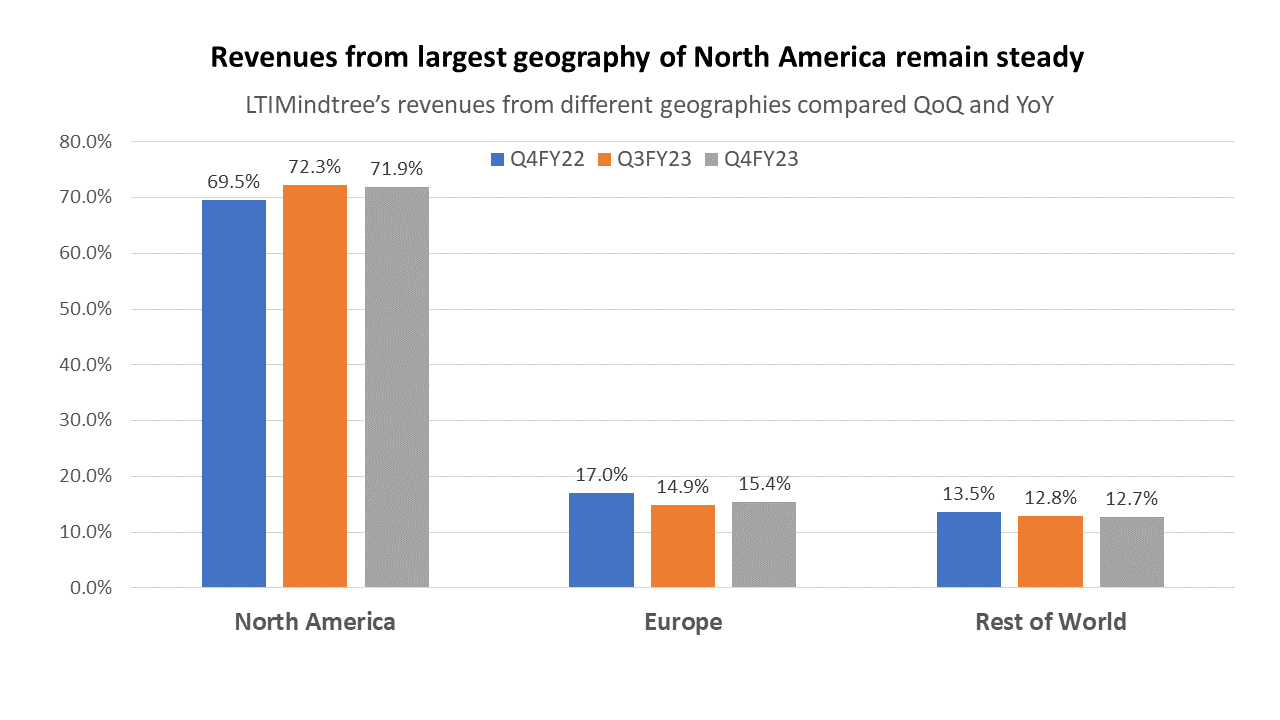

Among the various geographies that LTIMindtree operates in, it has maintained a steady revenue contribution from its largest territory of North America. In fact, it has grown by 2.4% on a YoY basis. This is significant as many other IT companies have seen a decline from North American clients. Even Europe, which is witnessing a slowdown in IT spends by clients has seen a decline of 1.6% only.

Conclusion

There are many factors that weigh in positively for LTIMindtree. The largest vertical, BFSI is growing, and the management expects this to grow further in coming quarters. It also shatters the narrative about slowing down in IT spends by North American Clients and the company has seen consistent growth in this geography.

Operationally, the company has achieved an optimum team size post the merger which will catalyse its growth and provide opportunities for larger deals in future. The stock is trading much lower than the peak price it had touched in end of 2021. It holds potential to rise again from the current levels to touch its all time high levels of around 7000 over the next one to two years.

ABOUT THE AUTHOR

Ketan Sonalkar (SEBI Rgn No INA000011255 )

Ketan Sonalkar is a certified SEBI registered investment advisor and head of research at Univest. He is one of the finest financial trainers, with a track record of having trained more than 2000 people in offline and online models. He serves as a consultant advisor to leading fintech and financial data firms. He has over 15 years of working experience in the finance field. He runs Advisory Services for Direct Equities and Personal Finance Transformation.

Note – This channel is for educational and training purpose only & any stock mentioned here should not be taken as a tip/recommendation/advice

You may also like: Weekly Update[/vc_column_text][/vc_column][/vc_row]

Recent Articles

Gold Price Prediction for Tomorrow: Key Levels, City Rates and Analyst Outlook for 31 July 2026

30 July 2026

Sensex Prediction for Tomorrow: Key Levels, Stock Picks and Analyst Outlook for 31 July 2026

30 July 2026

Nifty 50 Prediction for Tomorrow: Key Levels, Stock Picks and Analyst Outlook for 31 July 2026

30 July 2026

Stock Market Predictions for Tomorrow: Analysts Share Nifty Outlook for 31 July 2026

30 July 2026

Note: This blog is for information purpose only. Investments and trading are subject to market risks, read all scheme related documents carefully.

Reviews

Recent Posts

Gold Price Prediction for Tomorrow: Key Levels, City Rates and Analyst Outlook for 31 July 2026

Sensex Prediction for Tomorrow: Key Levels, Stock Picks and Analyst Outlook for 31 July 2026

Nifty 50 Prediction for Tomorrow: Key Levels, Stock Picks and Analyst Outlook for 31 July 2026

Stock Market Predictions for Tomorrow: Analysts Share Nifty Outlook for 31 July 2026

Stock Market Predictions for Tomorrow: Analysts Share Nifty Outlook for 30 July 2026

Popular this week

Gold Price Prediction for Tomorrow: Key Levels, City Rates and Analyst Outlook for 31 July 2026

Sensex Prediction for Tomorrow: Key Levels, Stock Picks and Analyst Outlook for 31 July 2026

Nifty 50 Prediction for Tomorrow: Key Levels, Stock Picks and Analyst Outlook for 31 July 2026

Stock Market Predictions for Tomorrow: Analysts Share Nifty Outlook for 31 July 2026

Stock Market Predictions for Tomorrow: Analysts Share Nifty Outlook for 30 July 2026

Uniresearch Global Pvt Ltd

Research Analyst

SEBI Registration Number — INH000013776

Uniresearch is a subsidiary of Univest Communication Technologies Private Limited

Company Address: Registered Address: Ground Floor, Unitech Commercial Tower 2, Block B, Greenwood City, Unit 1-3, Sector 45, Gurugram, Haryana 122003

Write to us : support@univest.in, compliance@univest.in

Verify on SEBI registry →RESEARCH ANALYST

Get SEBI Registered

advice on the stocks

trending today.

Get 3 FREE Trade Ideas

for Startups Accelerator 2024

Trusted by 1Cr Indians

Awarded No.1 by Economic Times