Balkrishna Industries- Detailed report

Updated: 12 Jan 2023 • 12:48 pm

Posted by:

High Conviction Long-Term Idea

Upside Potential: 45%

Positive Triggers: Raw material prices cooling, expansion plans, multi-country exports

Red Flags: Instability in the largest export market, change in raw material prices, and delay in expansion plans

About the Company

Balkrishna Industries Ltd is the flagship company of the Siyaram Poddar Group. It specialises in the manufacture of OTR (Off-The-Road) tyres, a niche tyre segment. These tyres are used in various sectors like agriculture (tractors, trailers, farm equipment), industrial and construction equipment (dump trucks, loaders, etc.), and for utility vehicles (golf carts, All Terrain Vehicles, etc.).

The company exports around 80% of its total production. Almost 50% of total production is sold in Europe while other major markets are North America, Asia, Middle East with a significant presence in South America, Africa, and Australia. It has four manufacturing facilities located at Bhiwadi & Chopanki in Rajasthan, Waluj in Maharashtra, and Bhuj in Gujarat.

What brings this company in focus?

Despite having seen a challenging situation in its key market, Europe, the company has consistently been able to improve its revenues in the last three quarters. The softening of raw material prices also builds optimism about the forthcoming quarterly results. In addition, the company’s expansion plan is expected to reap benefits over the next few quarters. On the technical charts, it has given a reversal signal hinting that the current downtrend has ended, and a new uptrend is about to begin.

Management commentary on the last quarter's performance

- “Looking at the current geo-political challenges across the globe especially in Europe, which is also our biggest market, there are strong headwinds. Despite these challenges during the quarter, the Company could deliver a good performance and registered sales volumes of 78,872 M”

- The current situation in Europe continues to be challenging and thereby may have an effect on our performance in H2FY23. The demand pattern has been relatively better in North America however recession fears have impacted the growth rates. India continues to be stably supported by a better economic environment backed by good monsoons.

- The recent price correction in raw materials and logistics costs bode well for our margin profile. However, as guided the benefits are expected to kick in from early Q4.

Data as on 10 Jan 2023

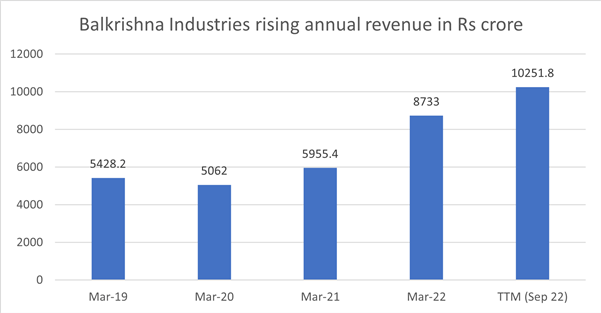

One of the factors that we look for while investing is consistency in the growth of the company over the past few years. It is also important that growth is also accompanied by profitability in equal measure. On this account, Balkrishna Industries' 3-year and 5-year CAGR for revenue growth and profitability stand out among the best in its industry.

Looking at the revenue growth over the past three years, FY21 ending Mar-21 had a YoY growth of 17.6%, and the subsequent year, FY22 saw a YoY growth of 46.6%. The TTM (trailing twelve months) data as on date points to another year of higher growth ending in FY23 if the subsequent quarters deliver accordingly. We expect the next quarters to be significant given the cooling of raw material prices as well as the fructification of expansion plans.

Expansion Plans

Bhuj

Commissioned the 50,000 MTPA brownfield tire plant at Bhuj in Q2FY23. The company expects a ramp-up in production in H2FY23. Project Capex Cost stands at Rs. 800cr.

Carbon Black and Captive Power plant

The management expects commissioning for 55,000 MTPA Carbon Black capacity along with Power Plant in December 2022. The Project of advanced carbon material for 30,000 MTPA will be commissioned in Q4FY23. Project Capex cost stands at Rs. 650cr.

Waluj

The Board had earlier intended to replace the Old Waluj plant with the newly commissioned Greenfield Plant, but given the subsequent business outlook, it was decided to continue operations at both plants along with the modernization of the Old Plant.

The Board has now decided to revert to its earlier decision of ceasing operations at the old plant. The earlier approved Capex of Rs. 350 crores for the modernization of the old plant will now be utillised at the new brownfield plant site to bring in economies of scale, which is expected to be completed by H1F124. The Waluj location will accordingly have an overall capacity of 55,000 MTPA at a single site

This will increase total production capacity to 360,000 MTPA by H1FY24 post-commissioning of the Waluj brownfield project.

Strong financial management

A key metric for ascertaining the financial health of a company is the ROCE (Return on Capital Employed). Balkrishna Industries has been consistently generating ROCE of above 20% for the past 4 years. This metric builds confidence in the overall ability of the company in prudently managing its finances.

The next quarter's results will confirm whether it will continue its growth trajectory from here on or would there be other factors that could adversely affect performance.

What do the charts say?

While there are many factors that are favourable towards investment, one check is whether the technical charts are supporting the fundamentals and if any positive news is being built into the price at this stage.

Balkrishna Industries had a stellar run in 2020 where it rose from levels of 700 to reach a high of around 2600 in October 2021, gaining more than 3X in price in that period. Post reaching this peak, the stock went into a downtrend testing the sloping long-term resistance line a few times. This week, for the first time after a year, the price has closed above this line supported by rising volumes.

This is an indication of a trend change and if this sustains, we could see the stock test levels of 2600, which would be the first resistance level. On crossing this level, the stock has the potential to touch levels of 3200 over a period of one year, implying a 45% upside from here.

ABOUT THE AUTHOR

Ketan Sonalkar (SEBI Rgn No INA000011255

Ketan Sonalkar is a certified SEBI registered investment advisor and head of research at Univest. He is one of the finest financial trainers, with a track record of having trained more than 2000 people in offline and online models. He serves as a consultant advisor to leading fintech and financial data firms. He has over 15 years of working experience in the finance field. He runs Advisory Services for Direct Equities and Personal Finance Transformation.

Note – This channel is for educational and training purpose only & any stock mentioned here should not be taken as a tip/recommendation/advice

You may also like: Weekly update for 31st December

Recent Articles

Stock Market Predictions for Tomorrow: Nifty at 24,615 After Iran Reversal as RBI Decision Day Arrives on 5 August 2026

4 August 2026

Intraday Stocks for Today: Bharti Airtel, SBI and Hindustan Zinc - Analyst Top Picks for 4 August 2026

4 August 2026

Crude Oil Price Prediction for Tomorrow, Tuesday 4 August 2026: Brent at $82 After 6% Single-Session Crash on Iran-US Peace Negotiations

3 August 2026

Natural Gas Price Prediction for Tomorrow, Tuesday 4 August 2026: MCX Natural Gas Falls to Rs 370/MMBTU as Iran Peace Reduces Strait of Hormuz Risk Premium

3 August 2026

Note: This blog is for information purpose only. Investments and trading are subject to market risks, read all scheme related documents carefully.

Reviews

Recent Posts

Stock Market Predictions for Tomorrow: Nifty at 24,615 After Iran Reversal as RBI Decision Day Arrives on 5 August 2026

Intraday Stocks for Today: Bharti Airtel, SBI and Hindustan Zinc - Analyst Top Picks for 4 August 2026

Crude Oil Price Prediction for Tomorrow, Tuesday 4 August 2026: Brent at $82 After 6% Single-Session Crash on Iran-US Peace Negotiations

Natural Gas Price Prediction for Tomorrow, Tuesday 4 August 2026: MCX Natural Gas Falls to Rs 370/MMBTU as Iran Peace Reduces Strait of Hormuz Risk Premium

Berger Paints vs Pidilite Industries: Which Stock Should You Track

Popular this week

Stock Market Predictions for Tomorrow: Nifty at 24,615 After Iran Reversal as RBI Decision Day Arrives on 5 August 2026

Intraday Stocks for Today: Bharti Airtel, SBI and Hindustan Zinc - Analyst Top Picks for 4 August 2026

Crude Oil Price Prediction for Tomorrow, Tuesday 4 August 2026: Brent at $82 After 6% Single-Session Crash on Iran-US Peace Negotiations

Natural Gas Price Prediction for Tomorrow, Tuesday 4 August 2026: MCX Natural Gas Falls to Rs 370/MMBTU as Iran Peace Reduces Strait of Hormuz Risk Premium

Berger Paints vs Pidilite Industries: Which Stock Should You Track

Uniresearch Global Pvt Ltd

Research Analyst

SEBI Registration Number — INH000013776

Uniresearch is a subsidiary of Univest Communication Technologies Private Limited

Company Address: Registered Address: Ground Floor, Unitech Commercial Tower 2, Block B, Greenwood City, Unit 1-3, Sector 45, Gurugram, Haryana 122003

Write to us : support@univest.in, compliance@univest.in

Verify on SEBI registry →RESEARCH ANALYST

Get SEBI Registered

advice on the stocks

trending today.

Get 3 FREE Trade Ideas

for Startups Accelerator 2024

Trusted by 1Cr Indians

Awarded No.1 by Economic Times