Bajaj Finance posts another excellent quarter with Q2FY23 results

Updated: 16 Nov 2022 • 5:38 pm

Posted by:

Bajaj Finance Limited is a non-banking financial company. The corporation has a sizable presence in both urban and rural India and has a diverse lending portfolio that includes lending to retail, SMEs, and commercial customers. The company has recently announced its Q2FY23 results, where Bajaj Finance was seen making a robust comeback. The company reported a strong quarterly result in line with their expectations, where they not only managed to report a balanced AUM growth but also excellent growth across operating parameters with a strong business momentum underway. The company saw a high double-digit PAT growth backed by a 31% YoY NII increase along with improving asset quality with an ROE greater than 20%.

Even on the technical charts, Bajaj Finance can be seen consolidating after a sharp up move following a steep correction in 2022. Though the stock has experienced a small correction after the post-announcement of their Q2FY23 results, brokerages remained bullish with the future prospects given its strong all round quarterly results. Therefore, let’s now analyse their Q2FY23 numbers and understand their current valuation while exploring future potential upside.

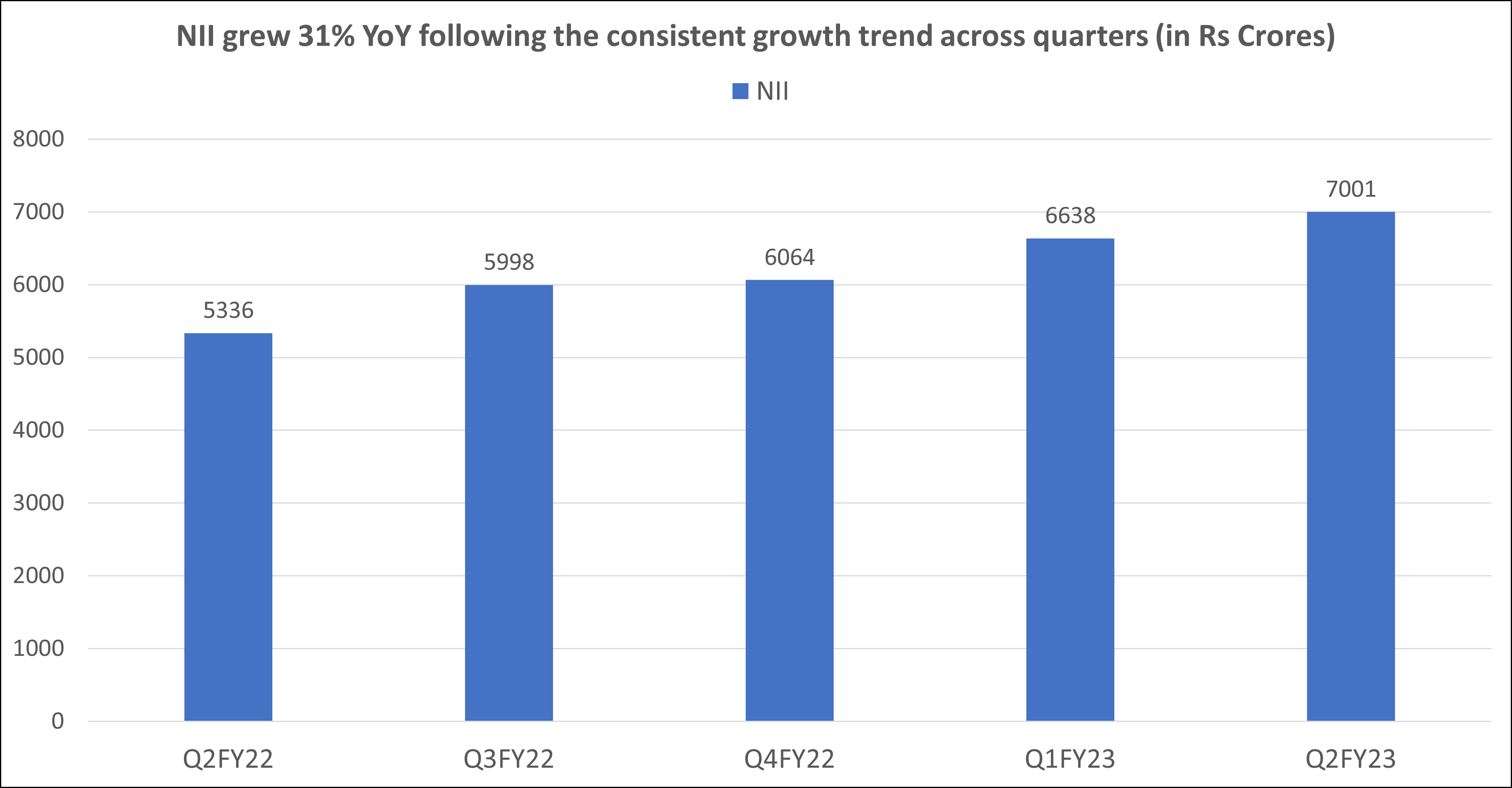

Bajaj Finance results Q2FY23: NII grew 31% YoY on back of healthy AUM growth

The result is driven by growth in consumer B2C finance and surge in SME lending. Bajaj Finance's NII increased 31% YoY to Rs 7,000 crores from Rs 5,337 reported in Q2FY22, driven primarily by robust AUM growth momentum. While the company's NIIs increased 5.4% QoQ from the Rs 6,638 crores reported in Q1FY23.

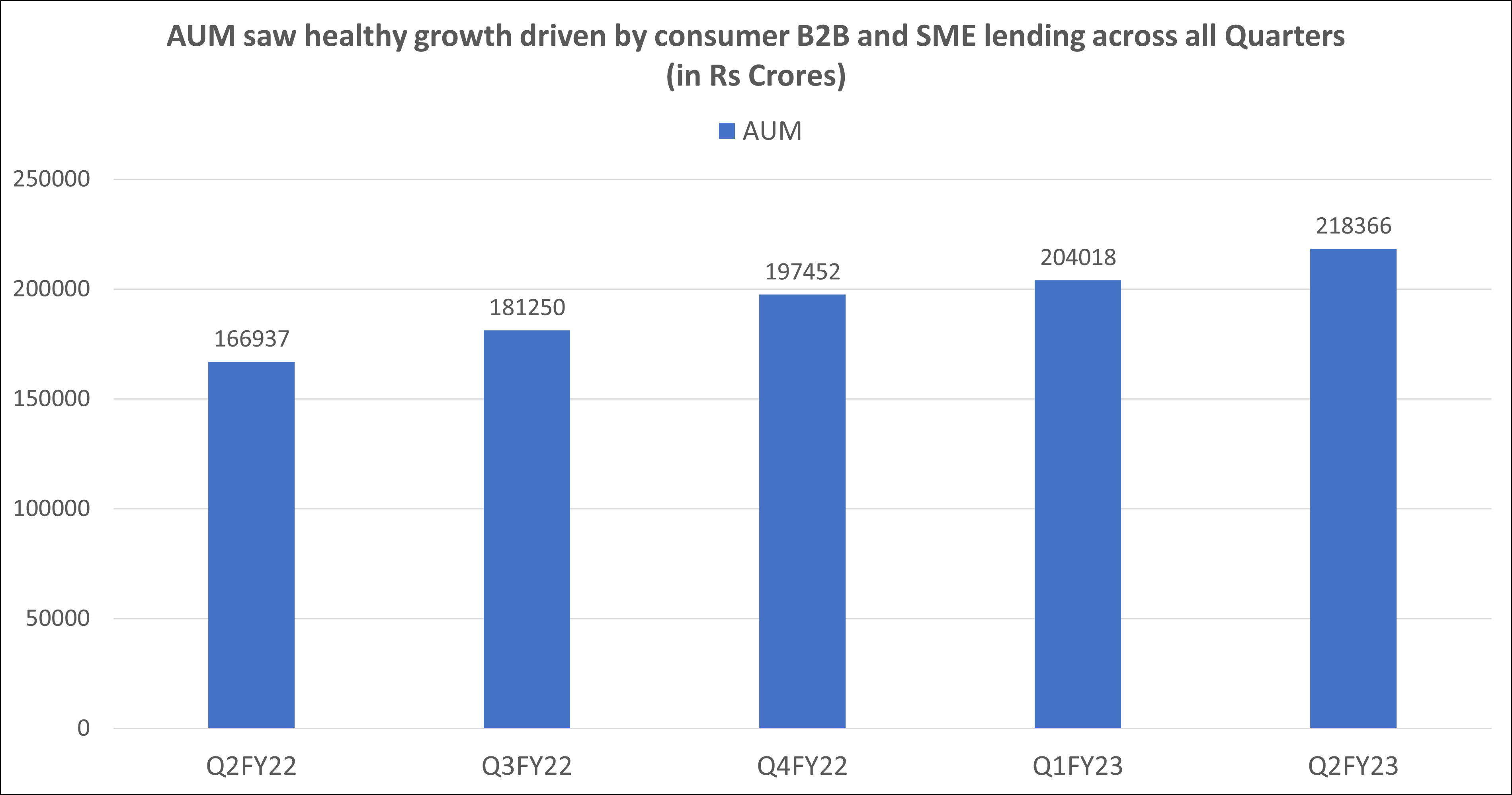

While AUM growth traction continued, rising 31% YoY to Rs 2,18,566 crore vs. up 7% QoQ. This increase was principally caused by a spike in SME lending as well as a 31% YoY, and 7% QoQ growth in consumer B2C finance. Mortgage growth also increased by 31% YoY and 8.3% QoQ to Rs 71092 crore. The preceding figure includes Rs 61191 crore in BHFL (HFC) AUM.

You may also like: Bajaj Auto Q2FY23

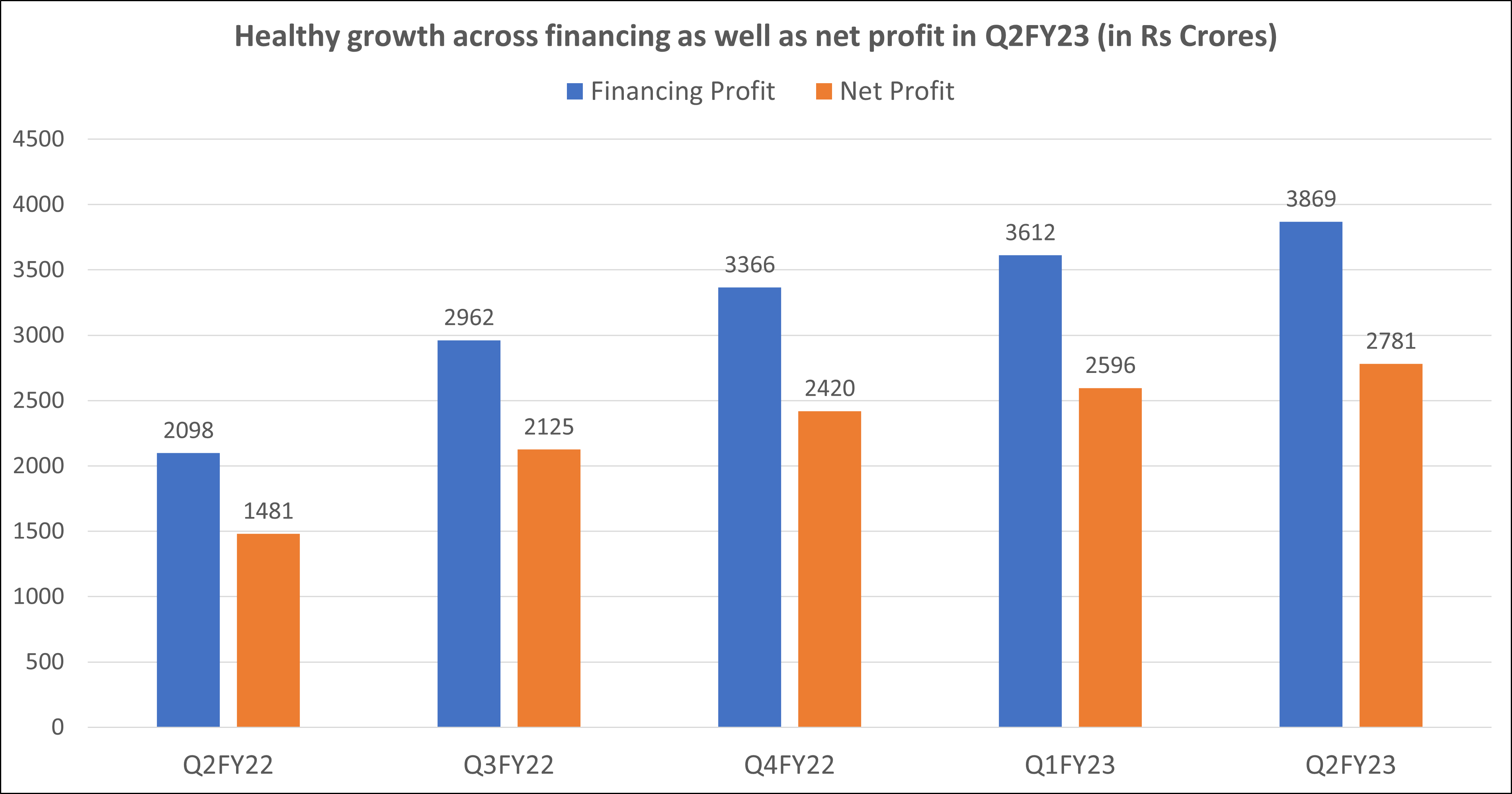

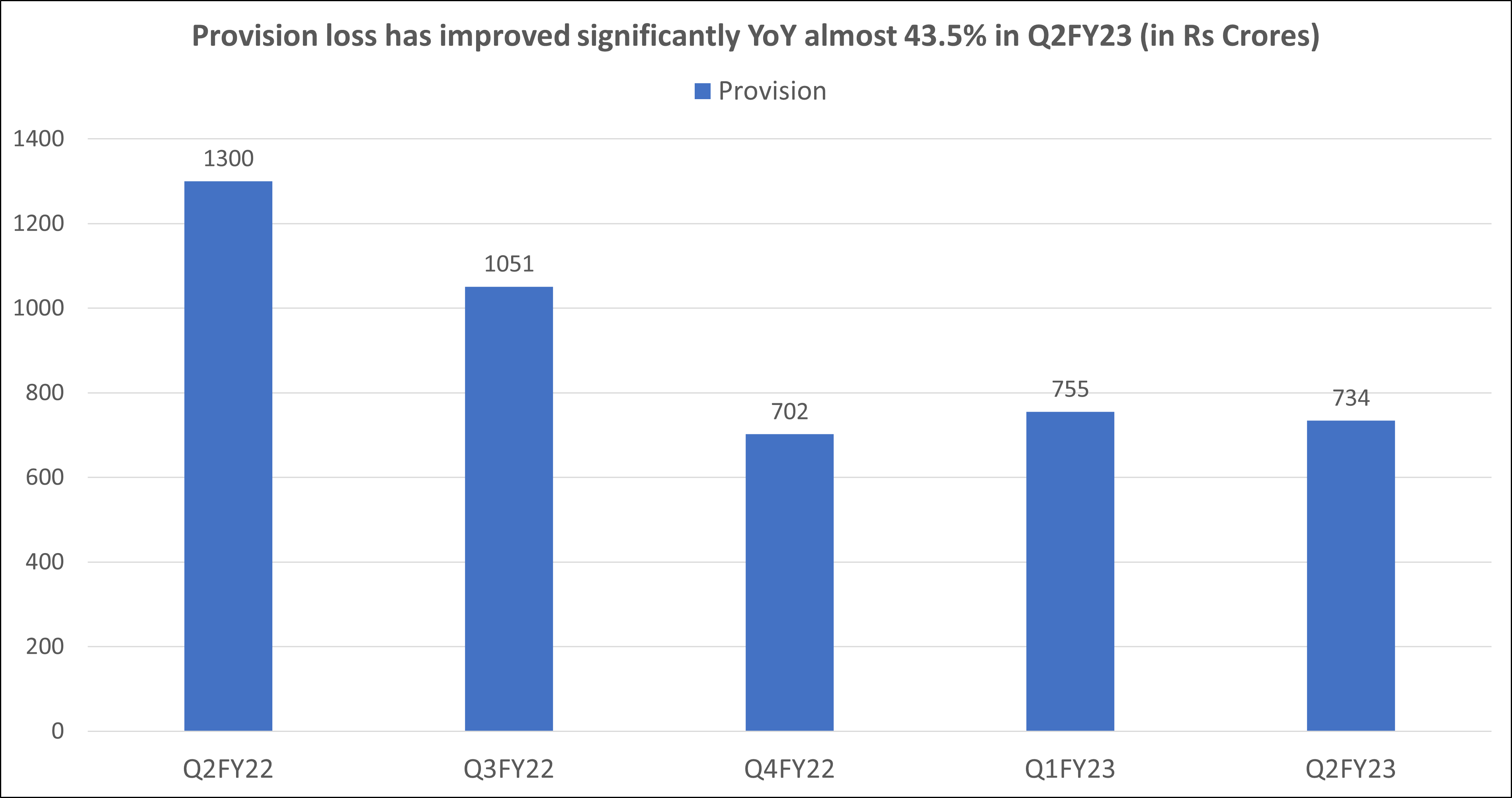

Bajaj Finance results Q2FY23: Highest ever PAT backed by 44% improvement in provision losses

With significant growth in net interest income (NII) and decreased loan loss provisions, Bajaj Finance reported its highest-ever quarterly consolidated net profit in Q2FY23. Its quarterly net profit increased 88% YoY to Rs 2,781 crores from Rs 1,481 crores reported in Q2FY23. While Net profit increased 7.1% sequentially from the Rs 2,596 crores reported in Q1FY23.

In terms of provisions, the lender's loan loss provisions decreased 44% YoY to Rs 734 crores in Q2FY23 from Rs 1,300 crores in the same quarter a year earlier. The company anticipates loan losses in FY23 to be between 1.35 and 1.45% of average assets. Additionally, as of the September quarter, it has a management overlay of Rs 1,000 crore.

Bajaj Finance results in Q2FY23: Improvement in asset quality with robust key ratios across business

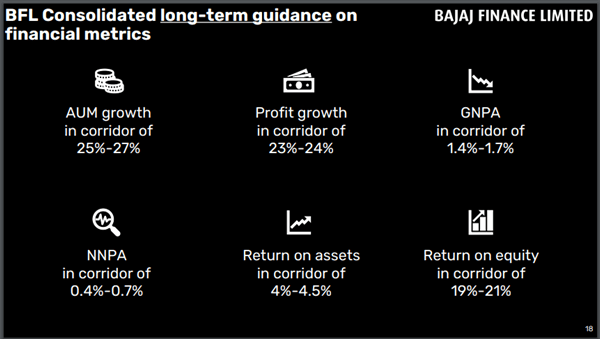

Throughout Q2FY23, the asset quality of Bajaj Finance strengthened. In comparison to 1.25% and 0.50%, respectively, in Q1FY23, the GNPA and NNPA were at 1.17% and 0.44%, respectively, as of Q2FY23. Additionally, as of September 30, 2022, the Deposits book totalled Rs 39,422 crore. The increase in net deposits during Q2 was Rs 5,320 crore. Lastly, deposits represented 22% of total borrowings. Further, in the medium term, the company is on track to achieve its long-term objective of 25% of consolidated borrowings from deposits.

At the end of September 2022, Bajaj Finance reported having 62.91 MM customers. Cross-sell franchise has a value of 36.39 MM. The company anticipates having 68–69 MM customers after the fiscal year.

(Source: Investor Presentation of Bajaj Finance for Q2FY23)

Univest View along with Technical Analysis:

Q2FY23 was an excellent first half for the Company across balance sheet growth, portfolio quality, and profitability. Strong momentum across all lines of businesses with secular AUM growth in the first half of FY23.

Additionally, Bajaj is on schedule to offer all of its products and services exclusively online by March 2023 and on mobile apps by January 2023. The App has already surpassed 26 MM online users. Web 2.0's first phase has been activated. The entire consumer application process for personal loans, EMI cards, co-brand credit cards, and two-wheeler marketplaces is now live on Print 1. Significant new feature improvements on Sprint 1 include services for credit cards, gold loans, EMI cards, new calculators, and an improved section for customer requests. Phase 2 will consist of three sprints. Sprint 1 will begin on August 31 as planned, followed by Sprint 2 on November 15 and Sprint 3 on January 31 of 2023.

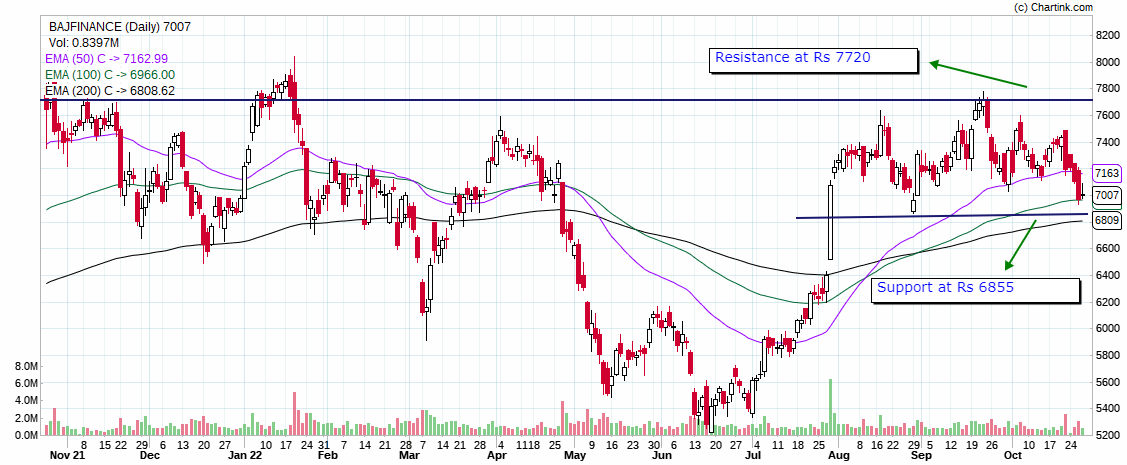

Even on the technical charts, the stock seems to be bullish on long term with 50 EMA above 100 & 200 EMA, despite share price correcting post Q2 results announcement. The reason for this minor down move was profit booking given the share price is already at a premium valuation which is justified by its fundamentals.

Whereas moving forward a key point to be noted is growth moderation from current levels and keeping a good track of the share price whether it tests resistance or moves below support. If the share price moves below its support level, investors can expect a retraction to 6,100 levels. Whereas, on Friday's closing the stock successfully made an inverted hammer candle, which is indicating a trend reversal. Therefore, it shall be interesting to note the direction of share price movement. While this consolidation may continue for one more week, investors should actively tract the price action.

ICICI Direct said, “Omnipresence strategy and organic momentum building up offers comfort on growth sustainability. The same holds the key for premium valuations. We marginally revise target price to Rs 8650 from Rs 8500.”

Whereas HDFC Securities said, “We make marginal upward tweaks to our FY23 earnings estimate (~2%) to factor in lower credit costs and maintain REDUCE with a revised TP of INR7,314.”

While on the Univest App, Bajaj Finance has a hold rating in both short as well long term, despite having a bullish stance on fundamentals as well as a long-term trend. Whereas over the short term, the company has a neutral rating, as stock is currently consolidating. Therefore, existing investors can remain invested unless the share crosses support from above, while fresh investors should wait for it to consolidate further before it breaks resistance with higher volume.

ABOUT THE AUTHOR

Ketan Sonalkar (SEBI Rgn No INA000011255 )

Ketan Sonalkar is a certified SEBI registered investment advisor and head of research at Univest. He is one of the finest financial trainers, with a track record of having trained more than 2000 people in offline and online models. He serves as a consultant advisor to leading fintech and financial data firms. He has over 15 years of working experience in the finance field. He runs Advisory Services for Direct Equities and Personal Finance Transformation.

Note – This channel is for educational and training purpose only & any stock mentioned here should not be taken as a tip/recommendation/advice

You may also like: Dabur, Tata Chemicals, BEL Q2FY23 results

Recent Articles

Nifty IT Prediction for Monday, 3 August 2026: Levels and Sector Outlook

31 July 2026

Nifty 50 Analysis: Technical Levels, Options Positioning, Sector Rotation and FII/DII Flows Ahead of Today's Session

31 July 2026

Bandhan Money Market Regular Monthly IDCW: NAV Today, Performance Review and Should You Invest?

31 July 2026

Gold Price Prediction for Tomorrow: Key Levels, City Rates and Analyst Outlook for 31 July 2026

30 July 2026

Note: This blog is for information purpose only. Investments and trading are subject to market risks, read all scheme related documents carefully.

Reviews

Recent Posts

Nifty IT Prediction for Monday, 3 August 2026: Levels and Sector Outlook

Nifty 50 Analysis: Technical Levels, Options Positioning, Sector Rotation and FII/DII Flows Ahead of Today's Session

Bandhan Money Market Regular Monthly IDCW: NAV Today, Performance Review and Should You Invest?

Gold Price Prediction for Tomorrow: Key Levels, City Rates and Analyst Outlook for 31 July 2026

Sensex Prediction for Tomorrow: Key Levels, Stock Picks and Analyst Outlook for 31 July 2026

Popular this week

Nifty IT Prediction for Monday, 3 August 2026: Levels and Sector Outlook

Nifty 50 Analysis: Technical Levels, Options Positioning, Sector Rotation and FII/DII Flows Ahead of Today's Session

Bandhan Money Market Regular Monthly IDCW: NAV Today, Performance Review and Should You Invest?

Gold Price Prediction for Tomorrow: Key Levels, City Rates and Analyst Outlook for 31 July 2026

Sensex Prediction for Tomorrow: Key Levels, Stock Picks and Analyst Outlook for 31 July 2026

Uniresearch Global Pvt Ltd

Research Analyst

SEBI Registration Number — INH000013776

Uniresearch is a subsidiary of Univest Communication Technologies Private Limited

Company Address: Registered Address: Ground Floor, Unitech Commercial Tower 2, Block B, Greenwood City, Unit 1-3, Sector 45, Gurugram, Haryana 122003

Write to us : support@univest.in, compliance@univest.in

Verify on SEBI registry →RESEARCH ANALYST

Get SEBI Registered

advice on the stocks

trending today.

Get 3 FREE Trade Ideas

for Startups Accelerator 2024

Trusted by 1Cr Indians

Awarded No.1 by Economic Times