Bajaj Auto Q2FY23 results were above expectation but saw falling exports

Updated: 16 Nov 2022 • 5:26 pm

Posted by:

Bajaj Auto is one of India's top two- and three-wheeler manufacturers. The company exports more two- and three-wheeled vehicles than any other entity in the nation and is part of the Bajaj Group.

The company announced its Q2FY23 results on 14th October’22, which saw the PAT/EBITDA growing 20% YoY. Despite being the largest exporter of two-wheelers from India, the company hasn't fared well on international markets in this quarter. Even in home markets, the performance is thought to be passable enough but isn't really up to par. With the current monthly wholesale rate at 65% of pre-covid levels, analysts believe Bajaj Auto is experiencing a rapid comeback in domestic 3W demand.

Despite all this, brokers have given the company a ‘Hold’ rating. Even the ongoing share buyback scheme, which boosted the share price, is now over. So, let's examine the Q2FY23 numbers as revealed by Bajaj Auto and determine what the future holds for them.

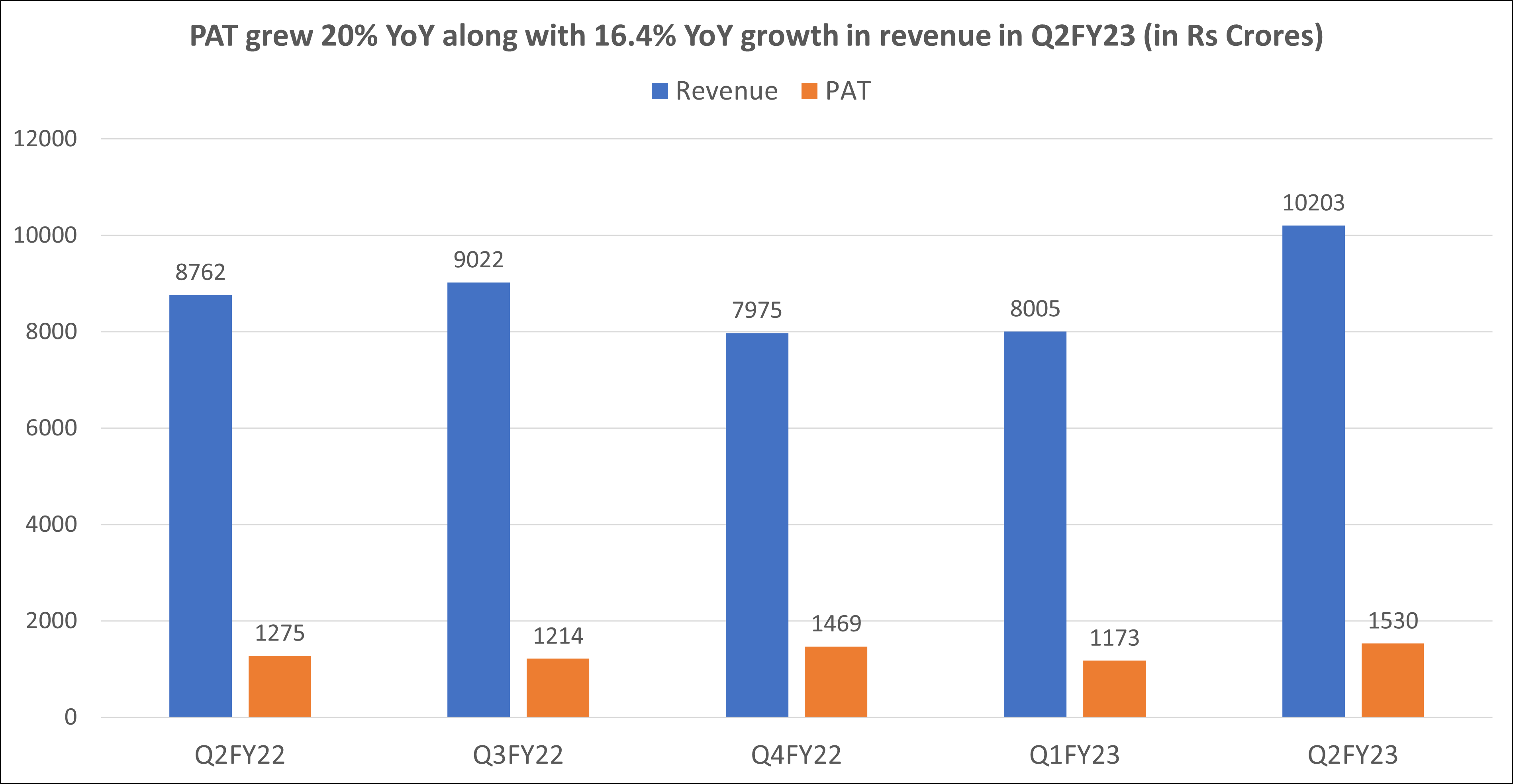

Bajaj Auto results in Q2FY23: Revenue grew 16.4% YoY and crossed Rs 10,000 crore for the first time

Bajaj Auto has reported a 20% YoY jump in net profit to Rs 1,530 crore in Q2FY23, beating analyst expectations. On a sequential basis, their PAT grew 30%, supported by price hikes, better product mix, cost efficiency, and better foreign exchange realization. Bajaj Auto’s revenue from operations jumped 16.4% YoY to Rs 10,202.8 crores from Rs 8,765 crores in Q2FY23. While revenue grew 27% QoQ from Rs 8,005 crores in Q1FY23.

Additionally, exports experienced a decline in the foreign markets as a result of unfavorable currency movement (which made imports more expensive), the supply of USD, and unfavorable economic conditions worldwide. "The second quarter was spectacular, with top-line and bottom-line results that broke records. As you are aware, there have been significant macroeconomic problems abroad as well as supply chain difficulties. Having said that, we anticipate Q3 to be better than Q2 due to improved supply chain visibility. Gains in volume and market share will be the company's main priorities in the coming months'', according to Rakesh Sharma, executive director of Bajaj Auto.

You may also like: Delta Corp share fell despite reporting highest ever revenue in Q2FY23

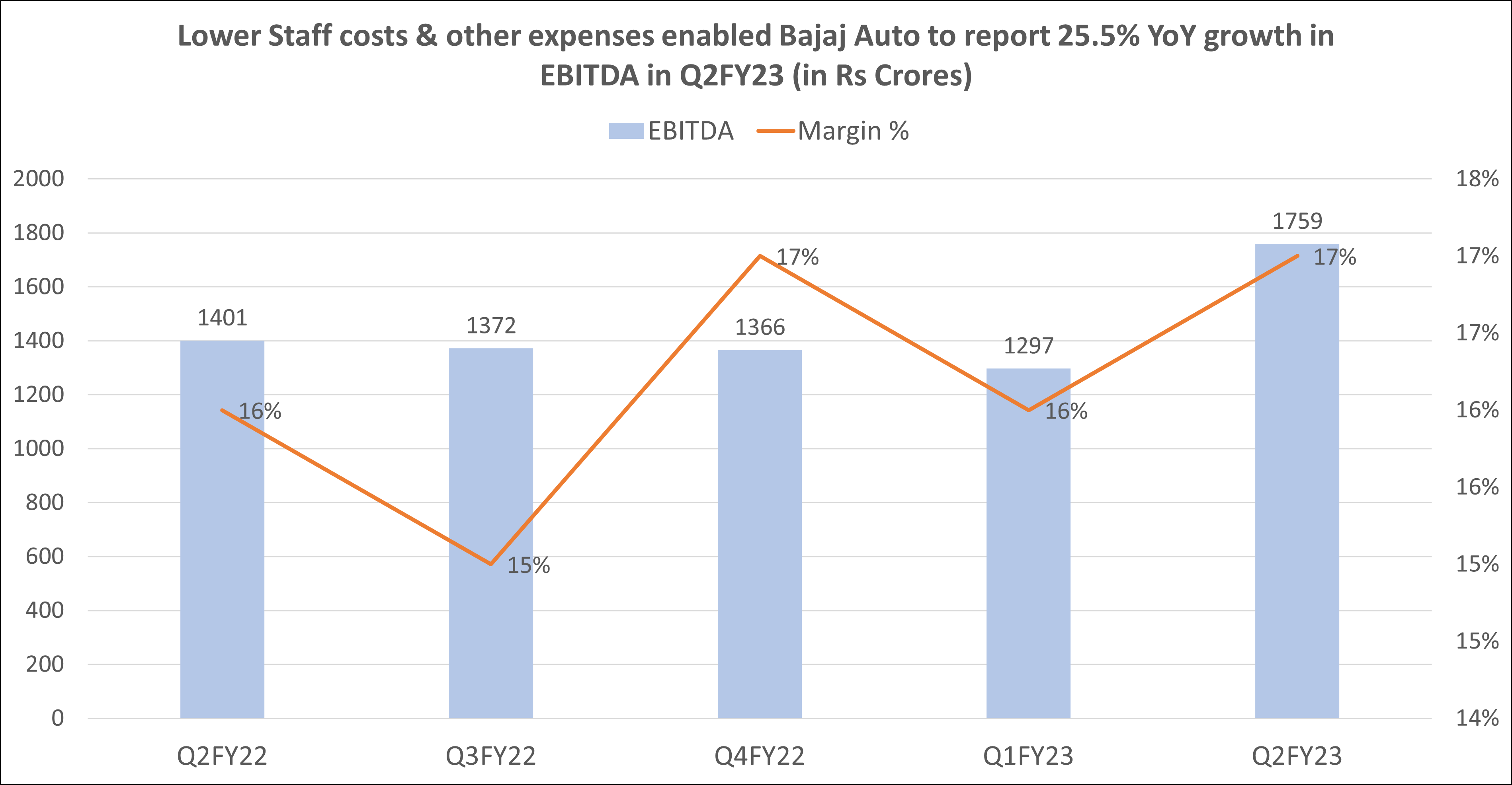

Bajaj Auto results in Q2FY23: Margins under recovery

Analysts think that Bajaj's good margins in Q2FY23 were a result of lower staff costs and other expenses. EBITDA for Bajaj Auto increased by 25.5% YoY to Rs 1,759 crore while EBITDA Margin YoY increased to 17.2% in Q2FY23. This was the highest quarterly EBITDA that Bajaj Auto has ever reported. Sequentially, EBITDA grew 36% from Rs 1,297 crores in Q1FY23.

"The reduced employee expense and other expenses, which decreased by 130 bps and 100 bps QoQ, respectively, along with a reduction in gross margins of 120 bps QoQ, compared to our assumption of a 15-bps increase in margin, were the reasons for the good margins", according to ICICI Securities analysts.

Bajaj Auto results in Q2FY23: Exports demand weak while EV planning robust

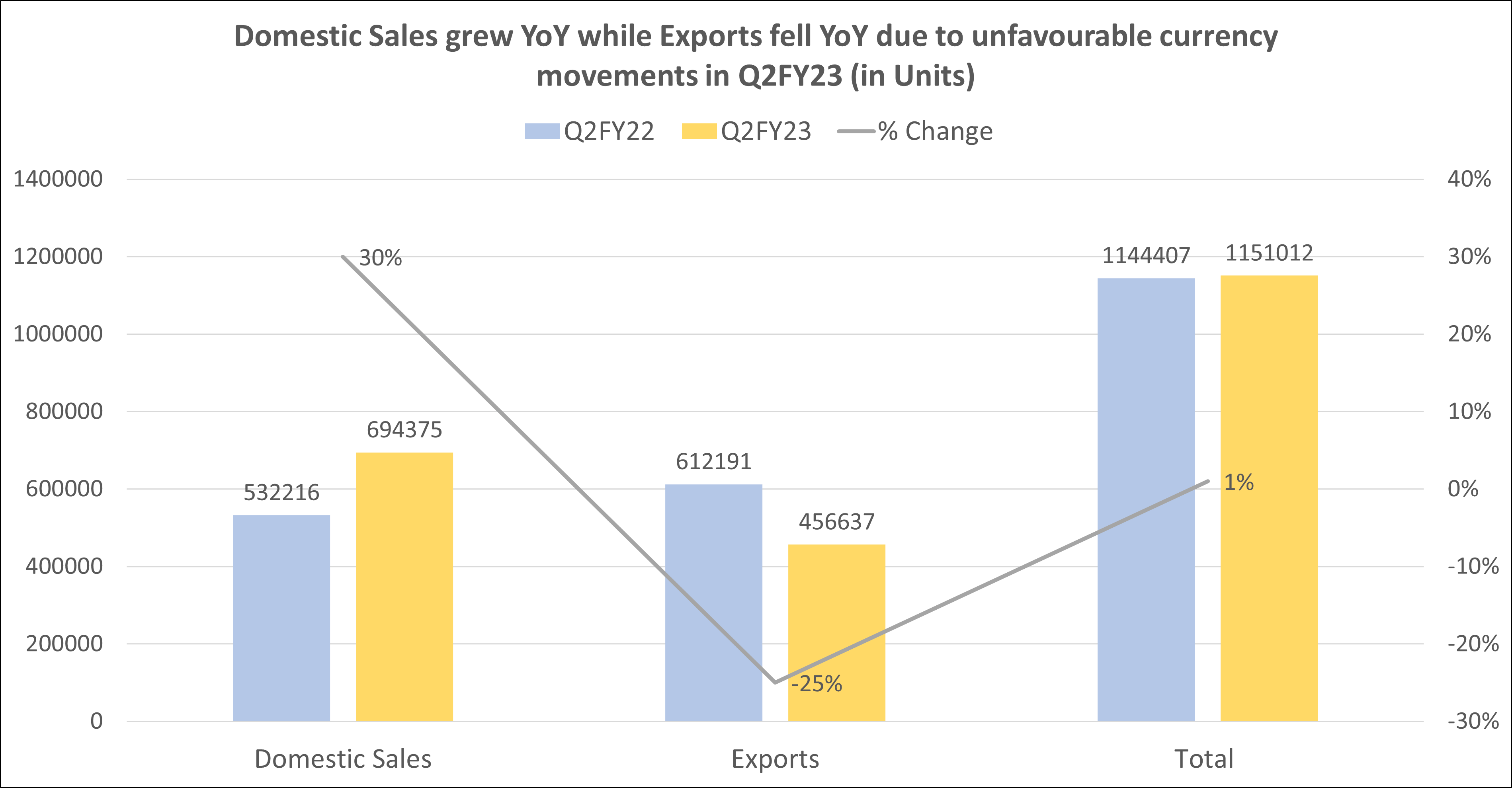

In comparison to 11.44 lakh units sold in Q2FY22 and 9.33 lakh units sold in Q1FY23, Bajaj Auto sold 11.51 lakh units in Q2FY23. The company's domestic sales in the two- and three-wheeler sectors nearly doubled from Q1FY23, which helped to offset the decline in exports. However, despite a 30% YoY increase in domestic sales, the overall sales for 2W and 3W only increased barely by 1% as a result of weak exports. The graph below demonstrates the same.

Due to the decrease in exports, Bajaj has been able to adjust its new stock distribution to the ASEAN and LAT-AM regions, where there is pent-up demand due to the preference for personal mobility that has emerged after the end of COVID-19. The current risk to demand in African countries like Egypt and Nigeria has thus been reduced in part by the revival of demand from Asian markets like the Philippines.

On the other hand, analysts anticipate that the electric 2-W space will ramp up volumes and the network will expand to 100 cities (expansion to 65 cities by FY23 end from current around 40 cities). The successful conclusion of electric-3W trials, with the introduction anticipated by the end of FY23E, will become those variables that will serve as crucial catalysts for price performance in the future. "In a market that is still significantly lower than pre-Covid, although recovering, Bajaj three-wheelers delivered an industry-leading performance, while retaining its strong position across segments; CNG does particularly well and is growing penetration," Baja Auto said in a statement. Last but not least, Capex for FY23 is anticipated to be Rs 7,500 crores, of which Rs 3400 crores is planned for H1. This amount will mostly go toward an EV plant and the building of a new location for the export of high-end vehicles.

Univest View along with Technical Analysis:

With Bajaj’s demand outlook bottoming out, the motorcycle industry is expected to grow in single digits. Chip supplies have started to improve from Sep’22, helping Bajaj Auto to build back its inventory to five weeks ahead of the festive season. Therefore, Bajaj’s market share would benefit over the long term from the premiumization trend, the opportunity in exports, and the potential sizable position in the Scooter market via EVs.

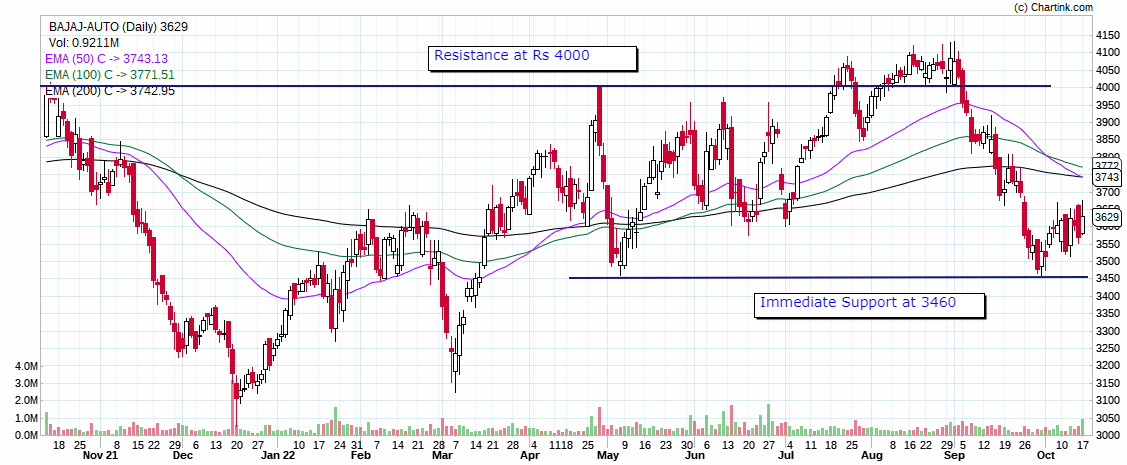

Coming onto technical charts, the Bajaj share is taking a major resistance at 4000-4070 levels, with immediate support at 3460. While the stock grew significantly from the beginning of 2022, it retracted back to its support in Q2FY23. Upon announcement of Q2FY23 results, there wasn’t much movement in stock as it has fallen slightly before the results & then gained a 1.6% on Monday. The 50 EMA line is close to crossing the 200 EMA line from above but if the share price continues to move up towards resistance, the EMA would come back on the favorable side.

Therefore, existing investors should hold onto their position as this quarter is considered to have bottomed out the demand & other problems & are expected to improve going forward. While new investors with a long-term view can take onto positions once Bajaj stock turns bullish on charts or close above its resistance.

"We maintain a 'hold' rating on Bajaj Auto primarily tracking the slower pace of volume recovery in both domestic and export markets, delay in electric -3-W launch,” brokerage firm ICICI Securities added.

Whereas Motilal Oswal said, “The stock’s valuation largely captures the expected recovery. BJAUT’s dividend yield of 5-5.5% would support the stock. We reiterate our Neutral rating with a TP of INR4,000/share.”

On the Univest app, the stock is in a sell zone on both the short as well as long-term time frames and it would be prudent to enter once the stock comes into the buy zone.

ABOUT THE AUTHOR

Ketan Sonalkar (SEBI Rgn No INA000011255

Ketan Sonalkar is a certified SEBI registered investment advisor and head of research at Univest. He is one of the finest financial trainers, with a track record of having trained more than 2000 people in offline and online models. He serves as a consultant advisor to leading fintech and financial data firms. He has over 15 years of working experience in the finance field. He runs Advisory Services for Direct Equities and Personal Finance Transformation.

Note – This channel is for educational and training purpose only & any stock mentioned here should not be taken as a tip/recommendation/advice

You may also like: IT firms saw their fundamentals rebounding in Q2FY23

Recent Articles

JioBlackRock Nifty 50 ETF: JioBlackRock AMC Launches Its First Exchange Traded Fund

4 August 2026

Stock Market Predictions for Tomorrow: Nifty at 24,615 After Iran Reversal as RBI Decision Day Arrives on 5 August 2026

4 August 2026

Intraday Stocks for Today: Bharti Airtel, SBI and Hindustan Zinc - Analyst Top Picks for 4 August 2026

4 August 2026

Crude Oil Price Prediction for Tomorrow, Tuesday 4 August 2026: Brent at $82 After 6% Single-Session Crash on Iran-US Peace Negotiations

3 August 2026

Note: This blog is for information purpose only. Investments and trading are subject to market risks, read all scheme related documents carefully.

Reviews

Recent Posts

JioBlackRock Nifty 50 ETF: JioBlackRock AMC Launches Its First Exchange Traded Fund

Stock Market Predictions for Tomorrow: Nifty at 24,615 After Iran Reversal as RBI Decision Day Arrives on 5 August 2026

Intraday Stocks for Today: Bharti Airtel, SBI and Hindustan Zinc - Analyst Top Picks for 4 August 2026

Crude Oil Price Prediction for Tomorrow, Tuesday 4 August 2026: Brent at $82 After 6% Single-Session Crash on Iran-US Peace Negotiations

Natural Gas Price Prediction for Tomorrow, Tuesday 4 August 2026: MCX Natural Gas Falls to Rs 370/MMBTU as Iran Peace Reduces Strait of Hormuz Risk Premium

Popular this week

JioBlackRock Nifty 50 ETF: JioBlackRock AMC Launches Its First Exchange Traded Fund

Stock Market Predictions for Tomorrow: Nifty at 24,615 After Iran Reversal as RBI Decision Day Arrives on 5 August 2026

Intraday Stocks for Today: Bharti Airtel, SBI and Hindustan Zinc - Analyst Top Picks for 4 August 2026

Crude Oil Price Prediction for Tomorrow, Tuesday 4 August 2026: Brent at $82 After 6% Single-Session Crash on Iran-US Peace Negotiations

Natural Gas Price Prediction for Tomorrow, Tuesday 4 August 2026: MCX Natural Gas Falls to Rs 370/MMBTU as Iran Peace Reduces Strait of Hormuz Risk Premium

Uniresearch Global Pvt Ltd

Research Analyst

SEBI Registration Number — INH000013776

Uniresearch is a subsidiary of Univest Communication Technologies Private Limited

Company Address: Registered Address: Ground Floor, Unitech Commercial Tower 2, Block B, Greenwood City, Unit 1-3, Sector 45, Gurugram, Haryana 122003

Write to us : support@univest.in, compliance@univest.in

Verify on SEBI registry →RESEARCH ANALYST

Get SEBI Registered

advice on the stocks

trending today.

Get 3 FREE Trade Ideas

for Startups Accelerator 2024

Trusted by 1Cr Indians

Awarded No.1 by Economic Times