Why Is Infosys Share Price Falling? Key Reasons & Infosys Share Price Target 2026

Updated: 1 Apr 2026 • 5:31 pm

Posted by:

Click Here — Get Free Investment Predictions from SEBI-Registered Analysts

Infosys share price is falling in 2026 due to a combination of weak revenue guidance, a one-time earnings miss from new labour code implementation, macro uncertainty from US tariffs affecting client spending, and broader IT sector sentiment driven by AI disruption fears. Infosys reported IT services revenue declining 3.5% quarter-on-quarter in Q4 FY25 — the company's weakest quarter since FY09 according to Goldman Sachs, which subsequently downgraded the stock from Buy to Neutral and cut its target price to Rs.1,530.

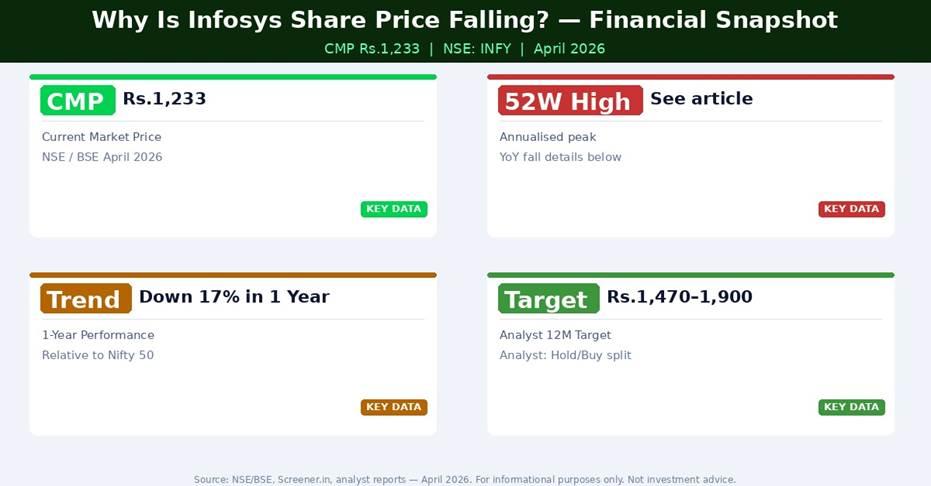

As of April 1, 2026, Infosys trades around Rs.1,233 on NSE — down approximately 17% over the past year and 21% from its February 2025 52-week high of Rs.1,922. The stock touched a 52-week low of Rs.1,307 in April 2025, with the current levels representing a meaningful recovery attempt from those lows.

About Infosys Limited

Infosys Limited is India's second-largest IT services and consulting company, headquartered in Bengaluru. It provides digital services including AI, cloud computing, data analytics, automation, enterprise transformation, and consulting to clients across more than 56 countries. With approximately 3,17,000+ employees, Infosys generated revenue of approximately $18.5 billion in FY25. The company is a constituent of the Nifty 50 and has been among the most widely tracked IT stocks in India for three decades.

Infosys financial snapshot — CMP Rs.1,233, Q4 FY25 weakness, analyst target range

Why Is Infosys Share Price Falling? — 6 Key Reasons

Tap to Access Best Research Pieces on Infosys at Univest

1. Q4 FY25 Revenue Decline — Worst Quarter Since FY09

Infosys reported a 4.2% quarter-on-quarter revenue decline in USD terms and a 3.5% decline in constant currency in Q4 FY25 — approximately 300 basis points below Goldman Sachs' and consensus estimates. Goldman Sachs characterised this as one of the company's weakest quarters since FY09. This significant miss relative to expectations triggered the Goldman downgrade from Buy to Neutral and a cut in target price to Rs.1,530 from Rs.1,790.

2. Weak FY26 Revenue Guidance: 0–3% CC Growth

Following the Q4 FY25 miss, Infosys guided for FY26 revenue growth of 0–3% in constant currency terms — a muted outlook reflecting macro uncertainty. Analysts had expected 3–6% CC growth. The guidance reflects client caution in the wake of US tariff announcements, slower discretionary spending, and continued pressure in the manufacturing and retail verticals — two segments where Infosys has significant exposure.

3. US Tariff Impact — Client Decision Deferral

US import tariffs announced in 2025 have created a chilling effect on discretionary technology spending across industries. Infosys, which derives approximately 85% of its revenue from North America and Europe, is directly exposed to this macro headwind. Clients in manufacturing, retail, and consumer sectors — facing direct impact from tariff-led cost increases — have deferred large transformation projects and reduced discretionary IT budgets. Management acknowledged that near-term revenue growth could outpace peers — but the baseline itself is low.

4. AI Disruption Fears — The Structural Overhang

A newer and potentially more structural reason for Infosys's share price pressure is the market's concern about AI disruption to traditional IT services. Advances in AI coding assistants and agentic AI platforms — including products from Anthropic, OpenAI, and Microsoft Copilot — are raising investor questions about whether human-intensive IT services revenue will be compressed over a 5-10 year horizon.

Infosys itself has been actively responding — investing in its Infosys Topaz AI platform, partnering with Citizens Bank for an AI-first Innovation Hub, and participating in the global generative AI ecosystem. But the market is pricing in uncertainty about whether AI headwinds or AI opportunities will dominate for Indian IT majors over the next 3-5 years.

5. One-Time Labour Code Charge in Q3 FY26

Infosys's Q3 FY26 PAT was impacted by a one-time charge related to India's new labour code implementation. This reduced operating margin to 18.4% in Q3 FY26, below the guided full-year range of 20–22%. While management reiterated the 20–22% EBIT margin guidance for the full year, the one-time charge disappointed investors expecting margin stability and raised questions about cost management.

6. Valuation Relative to Peers — Limited Edge

Infosys trades at approximately 21–22x forward P/E — broadly fair but not cheap given muted near-term growth. TCS commands a premium for stability; HCL Tech has shown positive earnings surprises. Infosys's valuation does not currently offer a meaningful discount to peers, reducing its attractiveness for momentum investors. This leaves the stock more vulnerable to negative guidance or macro news.

Infosys Financial Performance — Key Metrics

| Metric | Q4 FY25 | Q4 FY24 | YoY Change |

| IT Services Revenue (USD bn) | 2.597 | -2.3% YoY (CC) | Weak quarter |

| Revenue QoQ (CC) | -3.5% | Flat | Significant miss |

| Net Profit YoY | ~-17% YoY (estimates) | — | Labour code impact |

| FY26 Revenue Guidance | 0–3% CC YoY | Expected 3–6% | Below expectations |

| EBIT Margin Q3 FY26 | 18.4% | ~21% | Labour code hit |

| Large Deal TCV Q3 FY26 | $3.1 billion (67% net new) | — | Solid pipeline |

Source: Infosys earnings releases, Goldman Sachs research, Business Standard, INDmoney — April 2026.

Track Infosys's live fundamentals and FII activity on the Univest Screener.

Technical Analysis — Infosys Charts

- CMP: approximately Rs.1,233 — significantly below 200-day SMA

- 52-week high: Rs.1,922 (February 2025); 52-week low: Rs.1,307 (April 2025)

- The stock is in a well-established downtrend from Feb 2025 highs

- Key support: Rs.1,200–1,250 zone; Key resistance: Rs.1,400–1,450

- RSI near 40–45 — neutral, neither oversold nor overbought

Download the Univest iOS App or Univest Android App for live Infosys price alerts and SEBI-backed analyst commentary.

Infosys Share Price Target 2026 — Analyst Estimates

Subscribe to Univest Pro for Premium Infosys Research and F&O Setups

Short-Term (3–6 months)

With FY26 guidance already set at 0–3% CC growth, the near-term upside catalyst would be a Q4 FY26 results beat or any improvement in large deal ramp-up velocity. Short-term target range: Rs.1,200–1,400 depending on Q4 FY26 commentary.

12-Month Analyst Consensus

Analyst 12-month targets for Infosys range from Rs.1,470 (ICICI Securities, Hold) to Rs.2,200 (JM Financial, Buy). Goldman Sachs has a target of Rs.1,530 (Neutral), UBS at Rs.1,850 (Buy), HSBC at Rs.1,870 (Buy), Investec at Rs.1,575 (Buy). The median analyst target is approximately Rs.1,700–1,800, implying 35–45% upside from current levels.

Long-Term Target (2027–2030)

Long-term forecasts suggest Infosys reaching Rs.1,950–2,150 in CY2026 assuming mild demand recovery, and Rs.2,150–2,420 by 2027 with deeper cloud and AI service penetration. A scenario where Infosys successfully monetises its AI platform investments could drive earnings ahead of consensus and support valuations above Rs.2,500 by 2028-2030.

Will Infosys Share Price Recover?

Bull Case

Infosys has genuine strengths that the market is temporarily discounting: $3.1 billion in large deal wins in Q3 FY26 (67% net new business), a Rs.18,000 crore share buyback demonstrating management confidence, the Topaz AI platform gaining client traction, and the NHS contract in the UK providing long-duration revenue visibility. If AI adoption generates incremental revenue rather than replacing existing contracts — the thesis most bulls hold — Infosys's revenue quality actually improves.

Bear Case

The bear case is that Infosys is entering a multi-year structural slowdown as AI reduces the labour intensity of IT services. If discretionary spending remains constrained through FY27, and if AI productivity gains compress revenue per employee, the stock's earnings power may be permanently lower than historical levels — warranting a lower P/E multiple.

Conclusion

Infosys share price is falling in 2026 due to a rare convergence of Q4 FY25 revenue miss, muted FY26 guidance, US tariff-driven client budget deferrals, AI disruption concerns, and valuation lacking a discount to peers. The fundamental business remains strong — large deal wins, stable margins (ex-one-time charges), and AI investment are genuine positives. But the market needs visible evidence of demand recovery before re-rating the stock. Long-term investors may find current levels attractive relative to a 3-5 year horizon; short-term traders should wait for a guidance improvement catalyst.

Frequently Asked Questions

Why is Infosys share price falling in 2026?

Infosys share price is falling due to Q4 FY25 revenue declining 3.5% QoQ in CC terms — the weakest quarter since FY09. FY26 revenue guidance of 0–3% CC disappointed the market. Goldman Sachs downgraded the stock to Neutral and cut target to Rs.1,530. US tariff uncertainty is causing client decision deferrals, and AI disruption concerns are creating a structural overhang on IT sector valuations.

What is Infosys share price target for 2026?

Analyst 12-month targets for Infosys range from Rs.1,470 (ICICI Securities, Hold) to Rs.2,200 (JM Financial, Buy), with Goldman Sachs at Rs.1,530 (Neutral) and HSBC at Rs.1,870 (Buy). The median analyst target of Rs.1,700–1,800 implies approximately 35-45% upside from the current Rs.1,233 price. Long-term 2026-2030 forecasts range from Rs.1,950 to Rs.2,420 on demand recovery.

Is Infosys undervalued now?

At approximately 21x forward P/E, Infosys trades at a 12% discount to its 5-year average and broadly in line with its 10-year average — not cheap enough for value investors but not expensive relative to history. The stock becomes compelling if Q4 FY26 results show any positive guidance surprise, which would trigger analyst upgrades and institutional buying.

What is the Infosys 52-week high and low?

Infosys 52-week high was Rs.1,922 (hit in February 2025, when the stock rallied on strong deal wins and buyback announcement). The 52-week low was Rs.1,307 (hit in April 2025 after the Q4 FY25 results miss and Goldman Sachs downgrade). The current price of Rs.1,233 has recently breached the 52-week low — a technically bearish signal.

Disclaimer: This article is for informational and educational purposes only and does not constitute investment advice or a stock recommendation. Share prices and analyst targets mentioned are based on publicly available data as of April 2026 and are subject to change. Investing in stocks involves market risk — you may lose part or all of your capital. Always consult a SEBI-registered financial advisor before making investment decisions. Past performance does not guarantee future results.

Also Read

Why is KRBL Share Price Falling? Check Next Share Price Target

Why is Reliance Infrastructures Share Price Falling? Check Next Share Price Target

Why is Mahanagar Gas Share Price Falling? Check Next Share Price Target

Why is Happiest Minds Share Price Falling? Check Next Share Price Target

Recent Articles

Baroda BNP Paribas Equity Savings Fund Review: Plans, NAV, Returns and Portfolio Analysis 2026

3 August 2026

Baroda BNP Paribas Balanced Advantage Fund Review: Plans, NAV, Returns and Portfolio Analysis 2026

3 August 2026

Baroda BNP Paribas Yield Fund Review: Plans, NAV, Returns and Portfolio Analysis 2026

3 August 2026

Baroda BNP Paribas Business Cycle Fund Review: Plans, NAV, Returns and Portfolio Analysis 2026

3 August 2026

Note: This blog is for information purpose only. Investments and trading are subject to market risks, read all scheme related documents carefully.

Reviews

Recent Posts

Baroda BNP Paribas Equity Savings Fund Review: Plans, NAV, Returns and Portfolio Analysis 2026

Baroda BNP Paribas Balanced Advantage Fund Review: Plans, NAV, Returns and Portfolio Analysis 2026

Baroda BNP Paribas Yield Fund Review: Plans, NAV, Returns and Portfolio Analysis 2026

Baroda BNP Paribas Business Cycle Fund Review: Plans, NAV, Returns and Portfolio Analysis 2026

Baroda BNP Paribas Value Fund Review: Plans, NAV, Returns and Portfolio Analysis 2026

Popular this week

Baroda BNP Paribas Equity Savings Fund Review: Plans, NAV, Returns and Portfolio Analysis 2026

Baroda BNP Paribas Balanced Advantage Fund Review: Plans, NAV, Returns and Portfolio Analysis 2026

Baroda BNP Paribas Yield Fund Review: Plans, NAV, Returns and Portfolio Analysis 2026

Baroda BNP Paribas Business Cycle Fund Review: Plans, NAV, Returns and Portfolio Analysis 2026

Baroda BNP Paribas Value Fund Review: Plans, NAV, Returns and Portfolio Analysis 2026

Uniresearch Global Pvt Ltd

Research Analyst

SEBI Registration Number — INH000013776

Uniresearch is a subsidiary of Univest Communication Technologies Private Limited

Company Address: Registered Address: Ground Floor, Unitech Commercial Tower 2, Block B, Greenwood City, Unit 1-3, Sector 45, Gurugram, Haryana 122003

Write to us : support@univest.in, compliance@univest.in

Verify on SEBI registry →RESEARCH ANALYST

Get SEBI Registered

advice on the stocks

trending today.

Get 3 FREE Trade Ideas

for Startups Accelerator 2024

Trusted by 1Cr Indians

Awarded No.1 by Economic Times