TCS Q4 Results 2026 Date: Revenue, PAT, Dividend Expectations & Analyst Outlook

TCS Q4 Results FY26 — Board meeting scheduled April 9, 2026

Updated: 1 Apr 2026 • 11:28 am

Posted by:

The TCS Q4 results 2026 date has been officially confirmed as April 9, 2026. India's largest IT company enters its final quarter of FY26 under unusual pressure — the stock has lost 34% over the past year, Q3 FY26 profit fell 14% due to one-time charges, and the broader Nifty IT index is down over 20% year-to-date. Every number that comes out on April 9 will be picked apart.

What makes this quarter especially significant is that Q3's weakness was largely artificial — ₹2,128 crore in new labour law charges and ₹1,010 crore in legal provisioning distorted the reported profit. Q4 FY26 should strip those non-recurring costs out, revealing the true operational state of TCS heading into FY27. Investors are waiting for that clean read.

This article covers everything you need to know before April 9 — the official results date, revenue and PAT estimates, EBIT margin expectations, deal wins outlook, dividend possibilities, analyst ratings, and the five factors and five risks that will define how the market reads this quarter.

TCS Q4 Results 2026 Date — What the Official Filing Says

Get free investment predictions and live Q4 result alerts.

Tata Consultancy Services confirmed on March 25, 2026, through a BSE exchange filing that its Board of Directors will meet on Thursday, April 9, 2026, to approve the audited consolidated and standalone financial statements for Q4 FY26 — covering the quarter ended March 31, 2026. The board will simultaneously consider recommending a final dividend for FY26 for shareholder approval at the upcoming 31st Annual General Meeting.

The trading window for TCS's designated personnel was shut on March 24, 2026, and will remain closed until 48 hours after the results announcement — a standard governance protocol for a company of this standing.

Here is how the IT earnings season lines up for April 2026:

| Company | Q4 FY26 Results Date |

| TCS | April 9, 2026 |

| HCL Technologies | April 21, 2026 |

| Infosys | April 23, 2026 |

| Wipro | April 16, 2026 (expected) |

| Tech Mahindra | April 28, 2026 (expected) |

Source: BSE/NSE exchange filings, BusinessToday — April 2026. Expected dates may change.

Why Q4 FY26 Matters More Than a Typical Quarter

Q4 is not a routine earnings print for TCS this year. Three things make it genuinely pivotal.

First, the Q3 distortion. The December quarter's 14% YoY profit fall was almost entirely explained by ₹3,138 crore in combined non-recurring costs — ₹2,128 crore from government labour law changes and ₹1,010 crore in legal provisioning. Strip those out and the operational performance was reasonable. Q4 should print without those drags, giving analysts a clean baseline to assess true margins.

Second, the stock is at a multi-year low. TCS hit a 52-week low of ₹2,348 on March 23, 2026, just days before the results date announcement. The stock is down 25% year-to-date and 34% over the past year — a stunning fall for India's most widely held blue-chip IT stock. Any earnings beat, particularly on constant currency growth or deal TCV, could trigger a sharp mean-reversion rally.

Third, FY27 guidance commentary will be dissected word by word. TCS does not give formal quantitative guidance, but management's tone on deal conversions, demand from the US market, and the pace of AI adoption in client budgets will effectively set the stock's direction for the next two quarters.

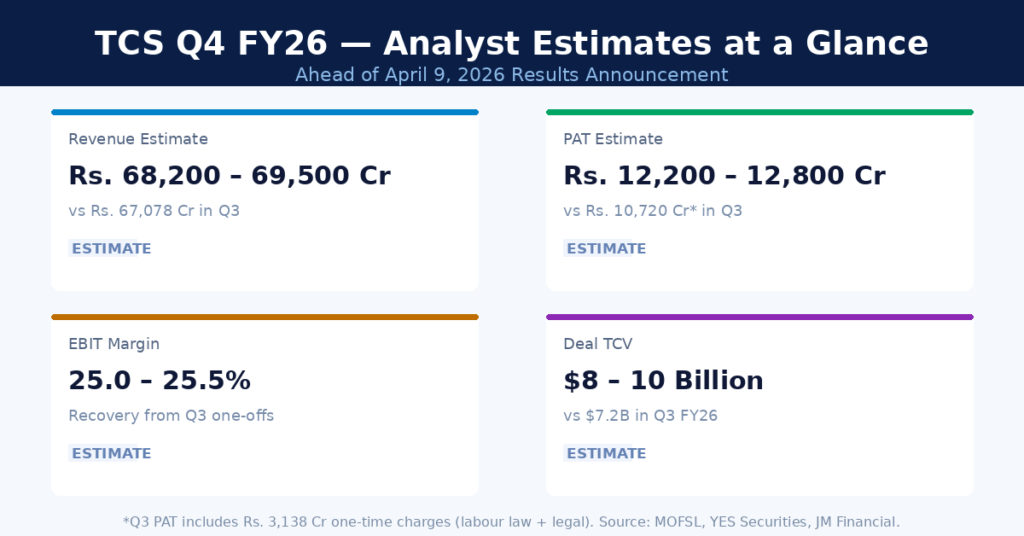

TCS Q4 FY26 Earnings Preview: Revenue, PAT & EBIT Estimates

TCS Q4 FY26 — Analyst consensus estimates across revenue, PAT, EBIT and deal TCV

Access the best IT sector research pieces

Motilal Oswal Financial Services (MOFSL) estimates TCS will report constant currency revenue growth of approximately 1.5% quarter-on-quarter in Q4, while YES Securities projects slightly higher growth of around 1.1% QoQ in CC terms, led by the BFSI and telecom verticals. MOFSL expects aggregate revenue for its IT coverage universe to grow 11.3% YoY in rupee terms for Q4, with EBIT growing 12.9% YoY.

On margins, MOFSL notes that TCS and Infosys are likely to see EBIT margins remain broadly stable in Q4, unlike HCL Tech which faces a 140 basis point contraction due to wage hike pressures. YES Securities estimates Q4 EBIT margins at around 25.3% for TCS — a recovery from the Q3 levels which were suppressed by one-time charges. ICICI Direct had earlier modelled EBIT margins of 24.8% for FY26 on a full-year basis.

| Metric | Q3 FY26 Actual | Q4 FY26 Estimate |

| Revenue (Rs. Cr) | 67,078 | ~68,200 – 69,500 |

| Net Profit / PAT (Rs. Cr) | 10,720* | ~12,200 – 12,800 |

| EBIT Margin (%) | ~22.1% (incl. one-offs) | 25.0 – 25.5% |

| CC Revenue Growth (QoQ) | +0.6% QoQ | ~1.1 – 1.5% QoQ |

| Deal TCV ($B) | $7.2B | $8 – 10B |

*Q3 PAT of Rs.10,720 Cr includes Rs.3,138 Cr in one-time charges. Source: MOFSL, YES Securities, JM Financial, NSE filings. Estimates — verify before investing.

JM Financial has an Add rating on TCS with a target price of Rs.2,660, while YES Securities carries a Buy with a target of Rs.3,162. On deal wins, analysts note that if TCS closes Q4 with TCV above $9 billion — closer to the $10 billion mark that some brokerages are pencilling in — it would signal strong demand pipeline heading into FY27 despite the macro uncertainty.

Check TCS fundamentals and screening data

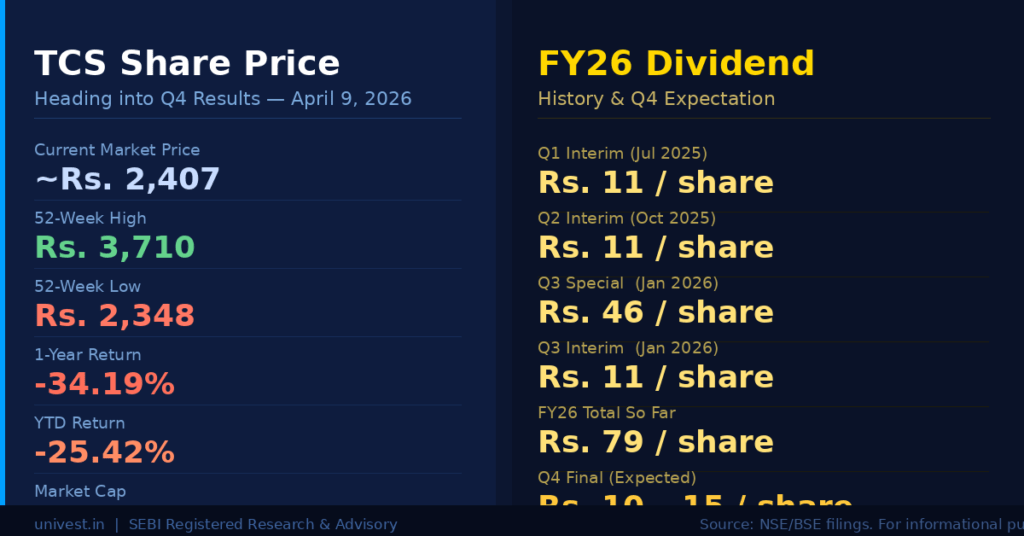

TCS Q4 FY26 Dividend: What Income Investors Are Watching

TCS has already been exceptionally generous in FY26. The company paid three separate dividends before Q4: a Rs.11 per share interim dividend in July 2025 (Q1), another Rs.11 per share in October 2025 (Q2), and in January 2026 — alongside Q3 results — an unusually large special dividend of Rs.46 per share plus a Rs.11 per share interim dividend. Total dividends paid in FY26 before the final payout: Rs.79 per share.

On April 9, the board will consider whether to recommend a final dividend for FY26. Historically, TCS has maintained a final dividend in the Rs.10–15 per share range during non-special years. However, given the stock's significant underperformance and TCS's consistently strong free cash flow generation, income investors are watching whether management uses the final dividend as a confidence signal to the market.

For investors who bought TCS at higher levels and have held through the correction, the dividend yield at current prices has improved meaningfully. At a CMP of Rs.2,407 and assuming a conservative final dividend of Rs.15 per share, the effective annual yield for FY26 would be approximately 3.9% on the total Rs.94 per share — not insignificant for a large-cap.

TCS Share Price Heading Into Q4 Results

TCS share price snapshot — CMP Rs.2,407, down 34% over one year, 52-week low at Rs.2,348

TCS shares were trading at approximately Rs.2,407 in late March 2026 — down 25.42% year-to-date, down 34.19% over the past year, and down 8.45% in the past month. The 52-week high was Rs.3,710 (March 2025), and the stock hit a 52-week low of Rs.2,348 just two days before confirming the results date on March 23, 2026. Market capitalisation stands at approximately Rs.8.68 lakh crore.

The five-year return is also negative at -21.46% — a sobering statistic for long-term holders, especially given TCS's status as India's most valued IT company for most of that period. The underperformance has been driven by a combination of global IT spending slowdowns, H-1B visa uncertainty impacting onsite delivery costs, and the broader narrative around AI disrupting traditional IT service models.

The technical picture shows TCS is deeply oversold by most indicators. A clean Q4 — particularly EBIT margins recovering to 25%+ and deal wins above $9 billion — could be the catalyst for a meaningful recovery. Conversely, any miss on guidance or signs of decelerating deal conversion would likely extend the downtrend toward Rs.2,200.

Get live TCS Q4 result alerts and daily stock research on the Univest iOS App and Univest Android App.

5 Factors That Will Drive TCS Q4 FY26 Performance

BFSI Vertical Recovery

Banking, financial services and insurance has historically contributed 31–33% of TCS revenue, making it the single most important vertical to watch. After a subdued Q3, any pickup in discretionary IT spending from US and UK banks — driven by compliance modernisation, AI-led core banking upgrades, or cloud migration programmes — will be a meaningful positive for Q4 topline.

EBIT Margin Normalisation Post One-Time Charges

The market is essentially expecting Q4 to demonstrate what TCS's true margins look like without the ₹3,138 crore in one-time Q3 charges. MOFSL expects margins to remain broadly stable QoQ while recovering sharply on a YoY comparison. A print at 25% or above would rebuild confidence in TCS's operational efficiency narrative heading into FY27.

AI Services — Threat or Revenue Driver

This is the defining question for the Indian IT sector in 2026. TCS has positioned its AI WisdomNext platform and agentic AI capabilities as a growth lever. In Q1 FY26, TCS reported accelerating demand for AI-led legacy modernisation and platform delivery models. Q4 management commentary will reveal whether those conversations have translated into sizeable contract wins, or whether AI is still at the pilot stage for most clients.

Currency Tailwinds

YES Securities noted that TCS's Q4 margins will be supported by currency tailwinds from a weaker Indian rupee against the US dollar. TCS earns the majority of its revenue in USD, GBP, and EUR. A weaker INR effectively boosts reported revenue in rupee terms even when constant currency growth is modest — providing a natural buffer to headline numbers.

Deal Pipeline Conversion and TCV

The Total Contract Value of deal wins is the most forward-looking indicator in TCS's quarterly results. The Q3 TCV came in at $7.2 billion. Analysts from MOFSL and YES Securities are expecting Q4 TCV of $8–10 billion. An incremental contribution from large multi-year deals — similar to the €550 million seven-year deal with Scandinavian insurer Tryg signed in Q2 — would be a material positive for FY27 revenue visibility.

5 Risks to Watch in TCS Q4 FY26

US Tariff Impact on Client IT Budgets

US President Trump's reciprocal tariff announcements triggered a sharp selloff in Indian IT stocks in early April 2025, with the Nifty IT index losing over 20% year-to-date. While TCS earns in services and is not directly exposed to goods tariffs, its US clients in manufacturing, retail, and automotive segments are under genuine budget pressure. Project deferrals and scope reductions from these sectors remain a live risk for TCS's revenue in Q4 and into FY27.

AI Cannibalisation of Traditional Service Lines

Generative AI tools are increasingly being embedded into software development, testing, and business process workflows — areas where TCS deploys a large portion of its 607,979-person workforce. While TCS is investing in AI capabilities, the structural risk of AI reducing per-unit billing in traditional fixed-price and time-and-material contracts is real and multi-year. MOFSL notes it does not yet see major evidence of deflationary shocks from AI implementation in current numbers — but concedes these are backward-looking data sets.

Muted or Cautious FY27 Guidance Commentary

TCS does not provide formal revenue guidance, but the management commentary following Q4 results will effectively function as guidance. If CEO K Krithivasan expresses caution on demand visibility in the US or signals client budget conservatism heading into FY27, the market will read it as a warning. Given the current geopolitical environment, the risk of a muted commentary is higher than in a typical year.

H-1B Visa Policy Uncertainty

TCS's onsite delivery model in the US depends heavily on H-1B visa availability. Any tightening of US immigration and work visa rules reduces TCS's operational flexibility, forces substitution with more expensive local hires, and increases cost of delivery in its largest market. This risk has been a persistent overhang on all Indian IT majors since late 2024.

Valuation Premium Despite Correction

Even after losing 34% in one year, TCS continues to trade at approximately 18–20x trailing twelve-month earnings — a premium to most global IT services peers. This limits the valuation cushion available if results disappoint. If EBIT margins come in below 24.5% or deal TCV falls short of expectations, there is limited valuation support at current levels to arrest further downside.

Analyst Ratings and Price Targets Ahead of Q4 Results

| Brokerage | Rating | Target Price (Rs.) | Key Thesis |

| JM Financial | Add | 2,660 | Margin recovery + AI deal wins |

| YES Securities | Buy | 3,162 | BFSI rebound + stable TCV momentum |

| MOFSL | Buy | NA disclosed | HCL Tech preferred; TCS margin stable |

| JPMorgan | Cautious | NA disclosed | Geopolitical headwinds + AI disruption risk |

Source: BusinessToday, MOFSL, YES Securities analyst notes — March/April 2026. For informational purposes only.

Conclusion

TCS Q4 results on April 9, 2026 are arguably the most watched earnings event in India's market calendar this quarter. After a noisy Q3 distorted by over Rs.3,000 crore in one-time charges, investors are looking for a clean number — ideally EBIT margins recovering above 25%, PAT in the Rs.12,200–12,800 crore range, and deal TCV printing above $8–9 billion.

The final dividend decision will serve as an additional signal from management. TCS has already paid Rs.79 per share in FY26, and any meaningful final dividend will reinforce the narrative that the company's balance sheet and cash generation remain intact even through this difficult period.

For investors holding TCS as a long-term position, April 9 is a pivotal date. For those considering fresh entry, the risk-reward at Rs.2,407 is asymmetric — meaningful upside if the quarter delivers, and limited downside support if it doesn't. Conduct your own research and consult a SEBI-registered advisor before making any decision.

Stay informed with Univest Blogs for Q4 results coverage on Infosys, HCL Tech, Reliance Industries, and more.

Frequently Asked Questions

What is the TCS Q4 results 2026 date?

The TCS Q4 results 2026 date is April 9, 2026. TCS officially announced on March 25, 2026, via a BSE exchange filing, that its board will meet on April 9 to approve Q4 FY26 financial results for the quarter ended March 31, 2026, and consider a final dividend for FY26.

What is the TCS Q4 FY26 PAT estimate?

Analysts estimate TCS Q4 FY26 net profit (PAT) in the range of Rs.12,200 to Rs.12,800 crore. This would represent a significant recovery from Q3's reported Rs.10,720 crore, which was weighed down by Rs.3,138 crore in one-time charges related to new labour laws and legal provisioning. Stripping those out, the underlying business remains broadly stable.

Will TCS declare a dividend in Q4 2026?

TCS is expected to recommend a final dividend for FY26 at the April 9 board meeting, subject to shareholder approval at the 31st AGM. The company has already paid Rs.79 per share in FY26 through three separate dividends — including a special Rs.46 per share payout in January 2026. Analysts are watching whether the final dividend matches or exceeds historical norms of Rs.10–15 per share.

What were TCS Q3 FY26 results?

TCS Q3 FY26 results showed revenue growth of 4.86% YoY to Rs.67,078 crore, but net profit fell 14% YoY to Rs.10,720 crore due to Rs.2,128 crore in new government labour law charges and Rs.1,010 crore in legal provisioning. These one-time items made Q3 optics weak, which is why Q4 is expected to deliver a meaningfully cleaner picture of margins and profitability.

What is TCS's share price ahead of Q4 results?

TCS shares were trading around Rs.2,407 in late March 2026 — down approximately 34% over the past year. The 52-week high was Rs.3,710 (March 2025) and the 52-week low was Rs.2,348 (March 23, 2026). The stock's market capitalisation stands at approximately Rs.8.68 lakh crore. The stock is under pressure from global macro uncertainty, AI disruption concerns, and US tariff headwinds.

Which brokerages have a Buy on TCS before Q4 results?

YES Securities has a Buy rating on TCS with a target price of Rs.3,162, citing potential BFSI vertical recovery and stable deal TCV momentum. JM Financial carries an Add rating with a Rs.2,660 target, expecting margin normalisation. MOFSL has a Buy on TCS but prefers HCL Technologies as its top large-cap IT pick. JPMorgan has flagged geopolitical headwinds and AI disruption as near-term risks.

When does Infosys announce Q4 results 2026?

The Infosys Q4 results 2026 date is April 23, 2026. The board will consider Q4 FY26 earnings and a final dividend on the same date. TCS kicks off the IT earnings season on April 9, followed by HCL Tech on April 21 and Infosys on April 23. Read the full Infosys Q4 preview on Univest Blogs.

Is TCS a good investment ahead of Q4 results?

This is a decision that depends entirely on your risk appetite, time horizon, and portfolio context. TCS is a fundamentally sound business with strong free cash flow, a diversified global client base, and a leading position in AI services. However, it faces genuine near-term headwinds from US tariff uncertainty, AI disruption risks, and a demanding valuation even after the 34% fall. Consult a SEBI-registered advisor before making any investment decision.

Disclaimer: Investment in the share market is subject to risk. This article is for informational purposes only. Conduct your own research before investing.

Recent Articles

Best Agrolife Q4 FY26 Results Preview & Earnings Expectations

Bhansali Engineering Polymers Q4 FY26 Results Preview & Earnings Outlook

Berger Paints Q4 FY26 Results Preview & Earnings Outlook

BEML Q4 FY26 Results Preview & Earnings Outlook

Belrise Industries Q4 FY26 Results Preview & Earnings Outlook

Recent Articles

Baroda BNP Paribas Equity Savings Fund Review: Plans, NAV, Returns and Portfolio Analysis 2026

3 August 2026

Baroda BNP Paribas Balanced Advantage Fund Review: Plans, NAV, Returns and Portfolio Analysis 2026

3 August 2026

Baroda BNP Paribas Yield Fund Review: Plans, NAV, Returns and Portfolio Analysis 2026

3 August 2026

Baroda BNP Paribas Business Cycle Fund Review: Plans, NAV, Returns and Portfolio Analysis 2026

3 August 2026

Note: This blog is for information purpose only. Investments and trading are subject to market risks, read all scheme related documents carefully.

Reviews

Recent Posts

Baroda BNP Paribas Equity Savings Fund Review: Plans, NAV, Returns and Portfolio Analysis 2026

Baroda BNP Paribas Balanced Advantage Fund Review: Plans, NAV, Returns and Portfolio Analysis 2026

Baroda BNP Paribas Yield Fund Review: Plans, NAV, Returns and Portfolio Analysis 2026

Baroda BNP Paribas Business Cycle Fund Review: Plans, NAV, Returns and Portfolio Analysis 2026

Baroda BNP Paribas Value Fund Review: Plans, NAV, Returns and Portfolio Analysis 2026

Popular this week

Baroda BNP Paribas Equity Savings Fund Review: Plans, NAV, Returns and Portfolio Analysis 2026

Baroda BNP Paribas Balanced Advantage Fund Review: Plans, NAV, Returns and Portfolio Analysis 2026

Baroda BNP Paribas Yield Fund Review: Plans, NAV, Returns and Portfolio Analysis 2026

Baroda BNP Paribas Business Cycle Fund Review: Plans, NAV, Returns and Portfolio Analysis 2026

Baroda BNP Paribas Value Fund Review: Plans, NAV, Returns and Portfolio Analysis 2026

Uniresearch Global Pvt Ltd

Research Analyst

SEBI Registration Number — INH000013776

Uniresearch is a subsidiary of Univest Communication Technologies Private Limited

Company Address: Registered Address: Ground Floor, Unitech Commercial Tower 2, Block B, Greenwood City, Unit 1-3, Sector 45, Gurugram, Haryana 122003

Write to us : support@univest.in, compliance@univest.in

Verify on SEBI registry →RESEARCH ANALYST

Get SEBI Registered

advice on the stocks

trending today.

Get 3 FREE Trade Ideas

for Startups Accelerator 2024

Trusted by 1Cr Indians

Awarded No.1 by Economic Times