Balaji Amines Q4 Results 2026: Date, Revenue, PAT & Analyst Outlook

Updated: 13 Apr 2026 • 6:25 pm

Posted by:

Balaji Amines (BALAMINES) Q4 FY26 results are scheduled for May 8, 2026, when the company's board of directors will approve the financial statements for the January-March 2026 quarter. Trading at Rs 2,050 as of April 2026 — down -28% from its 52-week high of Rs 2,950 — the stock has been under pressure alongside its peers in the Specialty Chemicals sector. This Q4 results preview covers the confirmed results date, analyst consensus estimates, five key performance factors, five risks to monitor, analyst ratings, and the complete share price outlook.

Balaji Amines's Q4 FY26 earnings will be watched for signals on the company's +12% volume YoY trajectory, and whether operating metrics are recovering toward normalised levels. This article provides a structured preview based on analyst consensus data and publicly available financial information.

Get free investment predictions on Univest.

Balaji Amines Q4 Results 2026 Date

The Balaji Amines Q4 FY26 results date is May 8, 2026. The board of directors will meet to approve the audited consolidated and standalone financial results for the quarter ended March 31, 2026, and the full year FY2025-26.

Here is a broader view of the Q4 FY26 results calendar for reference:

| Company | Results Date | Key Metric |

| [object Object] | April 9, 2026 (Declared) | FY27 revenue guidance, deal TCV |

| [object Object] | April 23, 2026 | CC growth guidance for FY27 |

| Bharat Electronics (BEL) | May 8, 2026 | Order book execution, EBITDA margin |

| Bharat Forge | May 10, 2026 | Global CV + defence execution |

| Balaji Amines | May 8, 2026 | See estimates below |

Why Q4 FY26 Matters

Q4 (January-March) is the final quarter of FY26, making it the most important earnings event of the year. Beyond the quarterly numbers, investors will receive: full-year FY26 financial summary, management commentary on FY27 business outlook, and the final dividend recommendation for FY26 shareholders.

For Balaji Amines specifically, Q4 FY26 captures the peak season dynamics of the Specialty Chemicals sector. Management's commentary on FY27 demand visibility will set the investment narrative for the next 12 months.

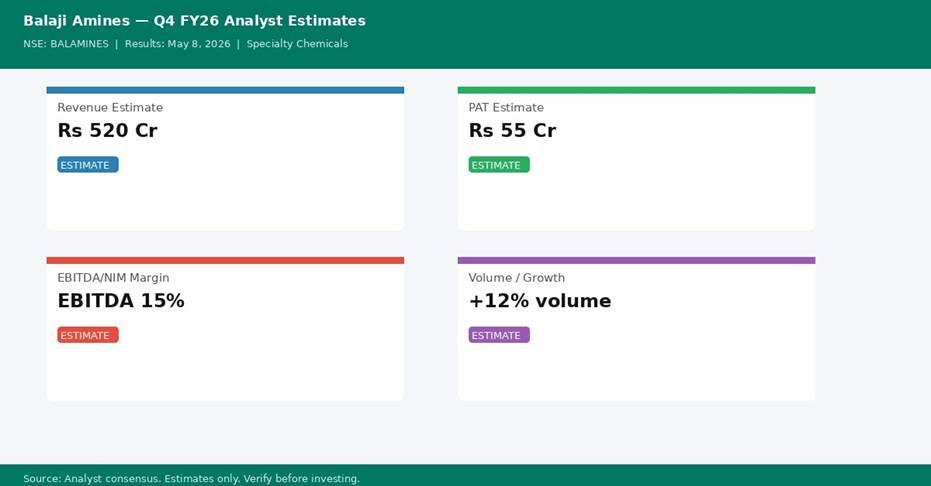

Balaji Amines Q4 FY26 Earnings Estimates

Access premium research on Univest.

Based on publicly available analyst consensus, here are the Q4 FY26 estimates for Balaji Amines:

| Metric | Q4 FY26 Estimate | Q3 FY26 Actual | Trend |

| Revenue | Rs 520 Cr | Rs 465 Cr | QoQ expected improvement |

| Net Profit (PAT) | Rs 55 Cr | Rs 48 Cr | Normalisation expected |

| Margin | EBITDA 15% | Q3 FY26 margin | QoQ trend |

| Volume / Growth Driver | +12% volume YoY | Prior quarter | YoY |

| Dividend (Expected) | Rs 6 (expected) | FY26 interim dividends | Final dividend |

Screen Balaji Amines live fundamentals on the Univest Screener.

Download the Univest iOS App or Univest Android App for real-time Q4 result alerts and analyst updates.

5 Key Factors Driving Balaji Amines Q4 FY26 Performance

1. Alkylamines Demand Recovery

Balaji Amines is India's largest alkylamines manufacturer. The agrochemical destocking cycle that suppressed demand through FY25-26 is approaching normalisation. Volume recovery in alkylamines for agricultural applications would be the primary Q4 catalyst.

2. Pharmaceutical and Water Treatment Demand

Non-agro applications (pharma intermediates, water treatment chemicals, and personal care) have been growing steadily. This segment diversification reduces dependence on the volatile agro chemical cycle.

3. Import Substitution

India's import of specialty amines from China and Germany has been progressively substituted by domestic manufacturers like Balaji. Formalization of import substitution in additional amine categories would expand addressable market.

4. Backward Integration Benefits

Balaji's backward integration into DMF (Dimethylformamide) and related products improves margin resilience by capturing value chain profits internally.

5. New Product Launches

The company has been developing new amine derivatives with higher application specificity. New product revenue contribution in Q4 FY26 would indicate portfolio expansion.

5 Risks to Watch in Balaji Amines Q4 FY26

Risk 1: Agrochemical Cycle Uncertainty

If global agro chemical destocking extends into FY27, Balaji Amines' volume recovery could be delayed.

Risk 2: China Pricing Pressure

Chinese amine producers export at subsidised prices, creating margin pressure for Indian manufacturers.

Risk 3: Crude Derivative Input Costs

Amines are derived from methanol and ethylene oxide, which are crude oil derivatives. Crude price spikes increase input costs.

Risk 4: Capacity Utilisation

Low utilisation during demand slowdowns increases per-unit fixed cost burden.

Risk 5: Environmental and Safety Compliance

Chemical manufacturing has high regulatory compliance requirements. Any incident or environmental violation would create operational and reputational risk.

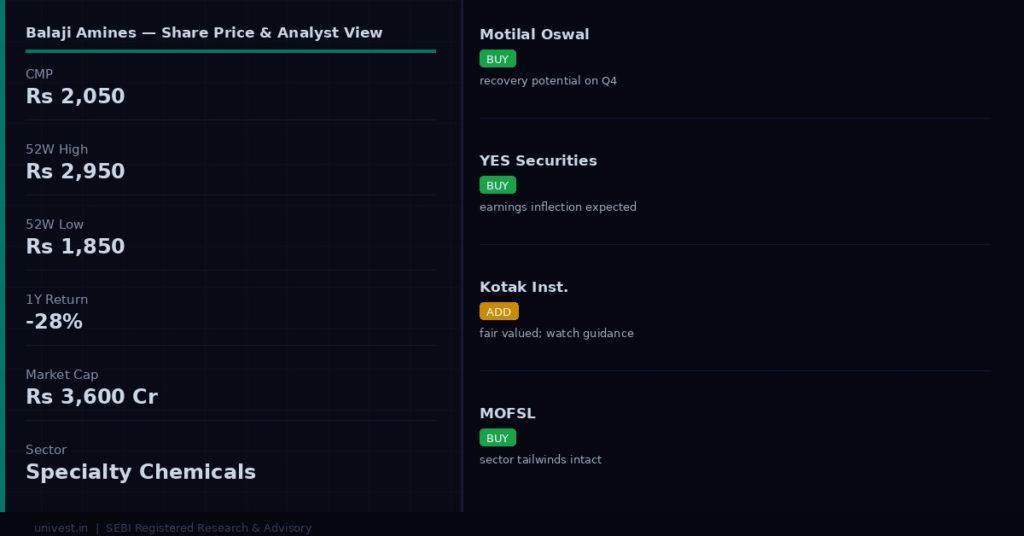

Balaji Amines Share Price and Analyst Ratings

| Parameter | Value |

| CMP (April 2026) | Rs 2,050 |

| 52-Week High | Rs 2,950 |

| 52-Week Low | Rs 1,850 |

| 1-Year Return | -28% |

| Market Capitalisation | Rs 3,600 Cr |

| Sector | Specialty Chemicals |

| NSE Ticker | BALAMINES |

Analyst ratings and target prices based on publicly available brokerage research:

| Brokerage | Rating | Target Price | Investment Thesis |

| Systematix | BUY | Rs 2,600 | Agro recovery to drive volume growth |

| Phillip Capital | ADD | Rs 2,400 | Import substitution story intact |

| Sharekhan | NEUTRAL | Rs 2,100 | Agro recovery timing uncertain |

Conclusion

Balaji Amines Q4 FY26 will be a key quarter for specialty chemical recovery. Volume above 12% growth and EBITDA margin above 14% would signal that the agro destocking cycle has peaked. At Rs 2,050, the stock offers reasonable value if the volume recovery thesis plays out.

Disclaimer: Investment in the share market is subject to risk. This article is for informational and educational purposes only and does not constitute investment advice. All financial data and analyst estimates are sourced from publicly available information including NSE/BSE filings and company investor relations pages. Verify all numbers before investing. Consult a SEBI-registered advisor before making investment decisions.

For more Q4 FY26 results previews, visit Univest Blogs.

Frequently Asked Questions

Q: When is Balaji Amines Q4 results 2026 date?

Balaji Amines Q4 FY26 results date is May 8, 2026. The board of directors will meet on this date to approve the quarterly and full-year FY26 financial results and consider recommending a final dividend.

Q: What is Balaji Amines Q4 FY26 revenue estimate?

Analyst consensus estimate for Balaji Amines Q4 FY26 revenue is Rs 520 Cr. Q3 FY26 actual revenue was Rs 465 Cr. Actual Q4 results may vary based on operating conditions.

Q: What is Balaji Amines Q4 FY26 PAT estimate?

Analyst consensus estimate for Balaji Amines Q4 FY26 net profit (PAT) is Rs 55 Cr. Q3 FY26 actual PAT was Rs 48 Cr. Estimates are indicative and not guaranteed.

Q: Will Balaji Amines declare a dividend in Q4 FY26?

Balaji Amines is expected to declare Rs 6 (expected) for FY26, subject to board approval at the May 8, 2026 board meeting and subsequent shareholder approval at the AGM.

Q: What is Balaji Amines current share price?

Balaji Amines is trading at Rs 2,050 as of April 2026, with a 52-week range of Rs 1,850 to Rs 2,950. The 1-year return is -28%.

Q: What were Balaji Amines Q3 FY26 results?

In Q3 FY26, Balaji Amines reported revenue of Rs 465 Cr and net profit (PAT) of Rs 48 Cr. The Q4 FY26 results on May 8, 2026 will provide a comparison to assess sequential and year-on-year trends.

Q: When do TCS and Infosys announce Q4 results 2026?

TCS declared Q4 FY26 results on April 9, 2026 (see the Balaji Amines earnings calendar table above). Infosys is scheduled to declare results on April 23, 2026. Both are covered in detail on Univest Blogs.

Q: Is Balaji Amines a good investment ahead of Q4 results?

This article does not constitute investment advice. Balaji Amines trades at Rs 2,050 with a 52-week range of Rs 1,850 to Rs 2,950. Analyst consensus targets and the Q4 FY26 estimates suggest monitoring the results date closely. Consult a SEBI-registered financial advisor for personalised investment guidance.

Recent Article

Techno Electric & Engineering Q4 Results 2026: Date, Revenue, PAT & Analyst Outlook

JBM Auto Q4 Results 2026: Date, Revenue, PAT & Analyst Outlook

Varroc Engineering Q4 Results 2026: Date, Revenue, PAT & Analyst Outlook

Hitachi Energy India Q4 Results 2026: Date, Revenue, PAT & Analyst Outlook

CG Power and Industrial Solutions Q4 Results 2026: Date, Revenue, PAT & Analyst Outlook

Recent Articles

Note: This blog is for information purpose only. Investments and trading are subject to market risks, read all scheme related documents carefully.

Reviews

Recent Posts

Standard Industries Share Price Forecast to 2030

Steel City Securities Share Price Forecast to 2030

STEEL EXCHANGE INDIA Share Price Forecast to 2030

Steel Strips Wheels Share Price Forecast to 2030

Steelcast Share Price Forecast to 2030

Popular this week

Standard Industries Share Price Forecast to 2030

Steel City Securities Share Price Forecast to 2030

STEEL EXCHANGE INDIA Share Price Forecast to 2030

Steel Strips Wheels Share Price Forecast to 2030

Steelcast Share Price Forecast to 2030

Uniresearch Global Pvt Ltd

Research Analyst

SEBI Registration Number — INH000013776

Uniresearch is a subsidiary of Univest Communication Technologies Private Limited

Company Address: Registered Address: Ground Floor, Unitech Commercial Tower 2, Block B, Greenwood City, Unit 1-3, Sector 45, Gurugram, Haryana 122003

Write to us : support@univest.in, compliance@univest.in

Verify on SEBI registry →RESEARCH ANALYST

Get SEBI Registered

advice on the stocks

trending today.

Get 3 FREE Trade Ideas

for Startups Accelerator 2024

Trusted by 1Cr Indians

Awarded No.1 by Economic Times